This year is passing so fast that sometimes I feel like I am unable to keep up with it. Once again it is time to share with you a progress I have made this quarter on my goals.

If you follow my blog, you may know that during my accounts rebuilt period I changed my course and made debt eliminating my priority number one. As Warren Buffett says if you want to be a successful investor you must stay out of debt. He even says to avoid credit cards entirely.

Why I haven’t listened to him earlier?

Debt elimination progress in 3Q 2013

I started working on my debt last quarter, so the results are not that bright as I would wish. I started to use all free money to eliminate debt. How I hate that debt! If it hasn’t existed I could have a plenty of free cash which I could use in the stock market! And today, when once again investors are dumping everything it creates great opportunities.

Today morning I watch CNBC, right at the moment when they spoke about Warren Buffett buying stocks during the worst panic in 2008 when everybody was selling. Today, just the dividends delivered him almost 10 billion of dollars!! In just five years!

The following chart shows my debt progress since the previous quarter.

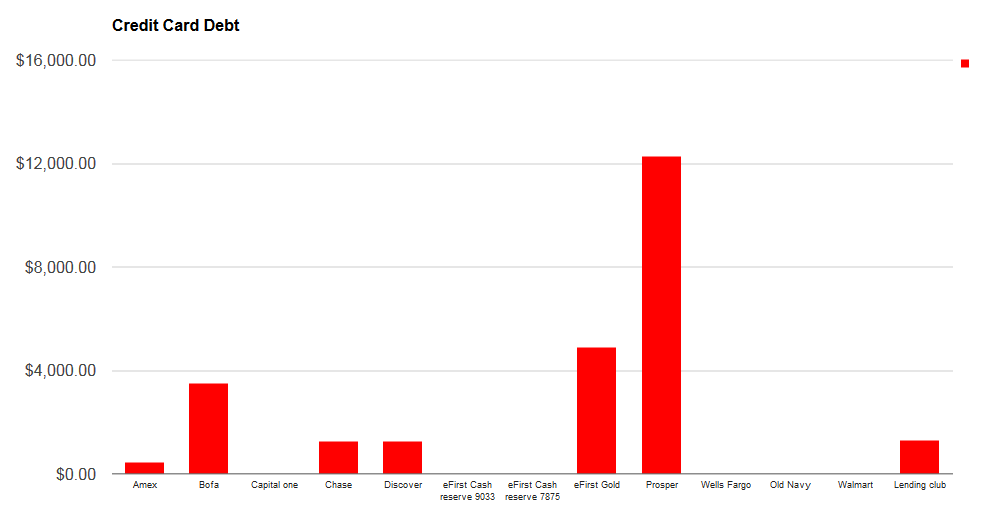

I made some progress on my debt which finally started showing retreat. The biggest achievement however was eliminating my debt on American Express card. This debt was literally killing me. I had to pay between 900 and 1600 monthly towards this debt and I had to use my reserves. Once my reserves were depleted I realized that this was a point to say a resolute no to this debt. I used refinancing plus paying all extra amount down and as of this writing I only owe 400 dollars. I am expecting eliminating that last piece by the end of the month.

But I am not out of the forest yet. Once my Amex is paid off, I will move on to paying other credit cards. But there will be no huge pressure. I will once again use all extra money to pay that debt off as quickly as possible.

The following chart show all my cards and debt I carry on. After my Amex is gone I will use a snowball method eliminating the smallest debt first and moving on.

As you can see, this goal shouldn’t be that difficult to reach.

My 3Q 2013 Investing Goal Results

Since I decided to attack my debt with my full financial power, I had to suspend my investing goals. Thus a little progress has been done. However, I still made money and increased my overall balances.

How could that be possible?

DIVIDENDS and options income!

My 3Q 2013 Dividend Income

Yes, my accounts were able to continue growing due to dividend income, which I diligently reinvest. I wasn’t able to reach my goal in dividend income and I might not be able to reach it by the end of the year due to my debt elimination priority, but I am satisfied with the result so far.

My goal was to reach $100 monthly in dividends at TD account.

I am currently at $84 a month. Not bad however.

My ROTH dividend income reached $63.99 a month.

You can follow and watch my dividend income on My Trades & Income page.

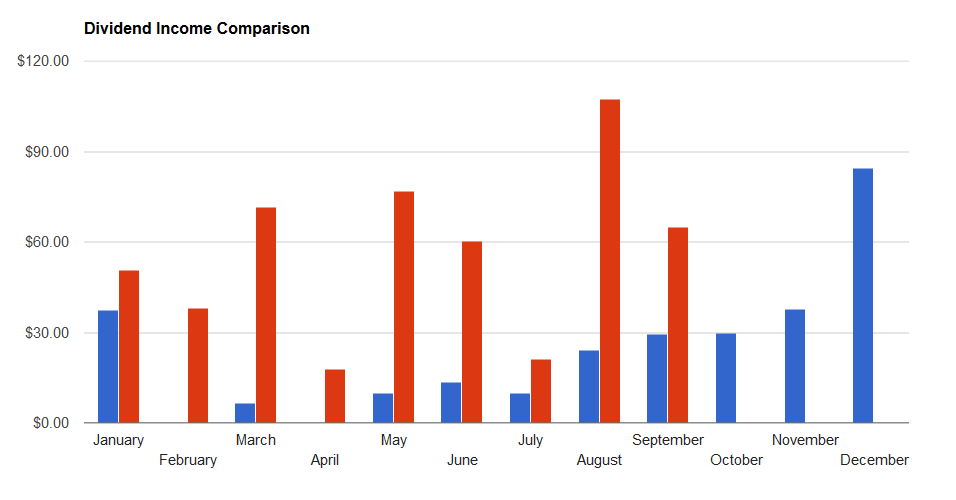

I like to see how my dividend income has been doing this year compared to my previous year. I started tracking it and the chart below shows a current year 2013 vs. 2012. I am satisfied with the growth of my dividend income.

(Note, the chart reflects dividend income on TD account only)

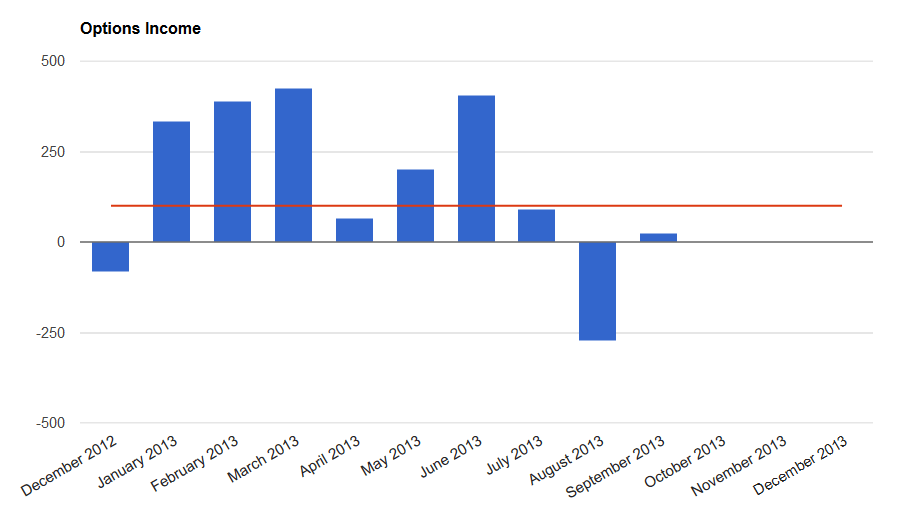

My 3Q 2013 Options Income

I reached my options income and continue successfully increasing it. Although in August I realized somewhat larger loss due to liquidating my ARR puts, it was still greatly offset by other income from options. I plan on selling covered calls and puts in the next quarter to increase my income beyond dividends.

My 3Q 2013 Overall Goals Summary

For the rest of the year I will however strive to continue investing as much as possible to reach my overall goal in investing:

Let me summarize my plan and goal for the future in steps:

- Pay off the debt and stay debt free.

- Re-build an emergency account.

- Raise TD account to $10,000 balance.

- Continue Dividend Growth Strategy on TD account and reinvesting all dividends. Reach min. $100 a month in dividend income.

- Continue covered calls and naked puts on TD account and reinvesting all proceeds, maintain or increase income to $100 a month.

- Once TD account reaches 10,000 dollars balance, deposit all available money in ROTH up to ROTH IRA limit. Everything beyond the limit will be deposited to TD account.

- Use Dividend Growth Strategy on ROTH and reinvest all dividends.

- Continue contributing $100 per month to Lending Club account and reinvest all proceeds.

Below is a review of all my accounts and investments:

I was able to increase a value of my accounts by 13%. Not a bad result considering that all my free money go towards debt and a very little to investments. My overall dividend income increased to 5.1% (from previous 4.9%)

You can continue watching my all open and closed trades on My Trades & Income page and check my holdings on My Holdings page.

My 3Q 2013 Lending Club Investment

My Lending Club account continues performing excellently. I am truly amazed and more than satisfied. The account is gaining a great momentum in growth and growing faster and faster. A portion of money in the account are my daughters for their college, missionary work (if they decide to go), or retirement.

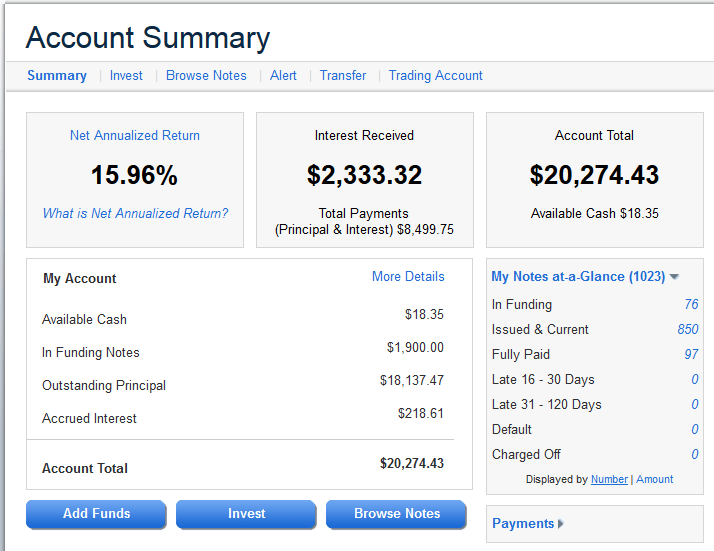

Currently this account reached 15.96% NAV or 12.81% XIRR.

The picture above shows my account at Lending Club. Note zero late or default notes as I continue actively managing this account and trying avoiding all notes which may potentially turn bad. You can also follow my Lending Club account on my Lending Club Holdings page.

I hope you had a great, successful, and prosperous saving, budgeting, investing and debt eliminating period as I had this 3rd quarter. I wish you all to have even better upcoming season.

Tell me how was your last investing, debt eliminating or money-saving period?

Would you recommend Lending Club as a potential retirement investment? I’m looking for a little bit of diversity in my retirement portfolio and it looks like you have had a whole lot of success with it. Do you enjoy the interactive nature of it?

If you are OK with the default rate you may suffer and associated risk then you can get really good results.

I still would split the money and invest partially in LC and partially in equities.

Thanks so much for responding. Sounds like I probably won’t get into LC until I have a little bit more available to invest. Thanks for the tip.

You can start with $500 dollars and test it for some time and see if it works for you or not. For some reasons I wrote about in my most recent post I decided to go away from LC and just keep 500 dollars in there as play money.

Thanks for the tip, it does sound like a good place to use some “speculation” money, where you get to experiment with your investment. It will still be a while before I get into it, but I’m looking forward to it. When I finally start I’ll probably come back to you asking for advice. Thanks for the help.

Sure, I will gladly help. But with current changes in the trading platform, it will be a piece of cake for you.

At the risk of sounding admonishing, I’d suggest first lowering the debt more before concentrating on stock. The (after tax) returns you get (unless those are very low interest cards) will far outweigh any dividend income. I’m betting you know that, but knowing it and doing it are different things. Debt payment often isn’t as FUN as investing, but it does generally have a higher return. It can be fun though – particularly when you pay off a large chunk at one time. I went though a similar issue myself recently.

The next thing I’d suggest is ignore the small debts. Go after the highest interest first since that is what is costing you money, and go after the debts that are a large loan to value – ie the more maxed-out ones. This will improve the credit score – which means you can refinance at better rates and improve your cash flow. Lowering the debt on a low interest and/or already low debt generally does little to help your score.

I agree. Knowing it and doing it are two different things and I fight this myself. However I am fully focused on eliminating the debt first.

Thanks for stopping by.

Martin, you are the Warren Buffett of Lending Club!

I see you have been investing for 3 years in lower grade notes and have 0 charge offs, 0 lates! That is unbelievable.

I have about the same amount of money in my account, have also been on there for about 3 years, and have 36 charge offs and 13 lates as we speak. My “lending club” net annualized return is about 10.75% so I am doing ok.

Awesome man..just awesome!

AA

AA, thanks, this is an amazing compliment and I honor it and treasure it. Thanks for stopping by and dropping such a great words.

I think you are OK. It is an amazing result you have. I manage my account very actively to avoid bad notes, but I usually sell them with a loss, but not as big as if the note goes default.

Martin, you are the Warren Buffett of Lending Club!

I see you have been investing for 3 years in lower grade notes and have 0 charge offs, 0 lates! That is unbelievable.

I have about the same amount of money in my account, have also been on there for about 3 years, and have 36 charge offs and 13 lates as we speak. My “lending club” net annualized return is about 10.75% so I am doing ok.

Awesome man..just awesome!

AA