For me, Thursday was a disappointment. I expected the market to gain some momentum after Wednesday’s rally like we saw in the past in similar situations after FED uplifting reports. Today, it didn’t happen and the whole day we were drifting down after morning large sell off.

This price action had an impact to a few trades I opened yesterday with today’s expiration and which I had to roll to keep them safe.

I had a bull put spread 2080/2085 against SPX which I moved lower to 2070/2075 when the stock market fell down to 2085 level and it looked like it would continue even lower. Later during the day the market moved higher, so at the end I didn’t have to roll this trade. But at that moment it didn’t look like that at all.

The second trade against SPX was a bull call spread 2090/2095 expecting the market to end above 2095. It didn’t happen either, so I had to roll this trade up and into a bear call spread at 2100/2105. That gave me some cushion and safety, but honestly, the rest of the day I was nervous fearing that the market would suddenly spike up and above 2100 and I would be toast.

So it wasn’t an easy trade for me at all.

Fortunately, both trades expired worthless today bringing a small profit. Unfortunately, those expected profits I hoped for yesterday vanished. But I finished positive and not with a loss.

Now, I only have one trade expiring tomorrow and that is a bull put spread against AAPL 125/120. So far, this trade is safe, but if the stock goes down significantly tomorrow I may either close this trade or roll it as well. As of now the trade is worth 3 cents, so I may close it commission free tomorrow or let it expire. That would depend on the market action tomorrow.

What is my expectation for tomorrow?

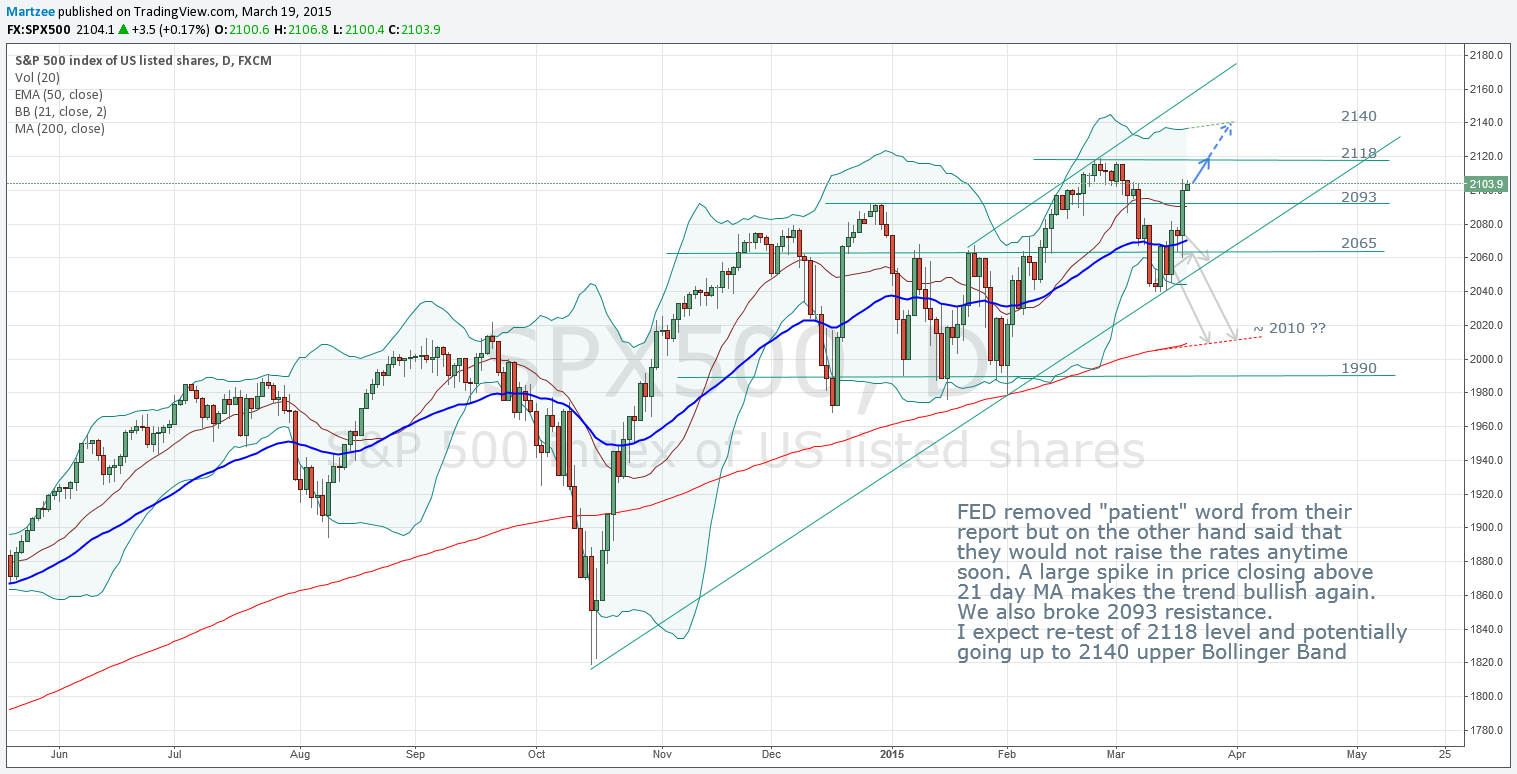

The overall trend is unchanged and we still should be heading up, although today’s price action revealed a lot of weakness in the market. I expect some weakness to continue tomorrow morning, but overall I expect Friday to end higher.

Tomorrow’s expected move

Bullish trend UP intact

Is a new rising channel forming?

There is also a potential that the market shows more weakness and continues back down to 2064 support. If the support won’t hold, then that would have a serious consequence to the overall trend and of course to our trades.

|

We all want to hear your opinion on the article above: No Comments |

Irving Kahn, a legendary investor, and student and later coworker of Benjamin Graham, once said about speculators and investors in Wall Street:

Irving Kahn, a legendary investor, and student and later coworker of Benjamin Graham, once said about speculators and investors in Wall Street:

Recent Comments