Many future planner advisers who were trained to sell you their 401k plans to get their share of fees will be outraged if you tell them that 401k plans is a legal way how the financial industry is robbing us from our money and that there are better ways to save money for retirement.

It is stunning how far this industry gambling with our future could go convincing you that you are basically an idiot who cannot take care of his own money so you need them to do it for you.

I bet you have heard many times that Americans have nothing saved, or haven’t saved enough for retirement. While a few decades ago, having saved 50,000 to 100,000 dollars could be enough for retirement, today they tell you that you have to amaze million of dollars to retire. Have you ever tried those retirement calculators online? What was the number they threw at you? One million dollars? Three million dollars?

And even if you save every penny during your productive life, do not buy a house, do not buy a car, do not start a family, but save everything and thanks to enormous, hidden, and compounded fees, and their poor performance you find yourself 30 years later broke, they will be bold in telling you that you haven’t saved enough.

There are many myths people are told to believe about their 401k plans. Some are so outrageous that I can’t believe it didn’t come to me earlier what lies we are told when it goes about our future well being.

Let’s review a few myths and lies we are regularly told to believe and which made me to stop contributing to my 401k.

· People do not have enough knowledge, time, or capacity to invest on their own.

This claim is like saying that you are stupid enough to drive a car so you have to hire a driver for yourself. If you are really so lazy to learn a few simple basics about investing, they yes, you deserve to be robbed by the 401k industry.

Look at it this way. What you do in 401k? You buy mutual funds. What the mutual funds do with your money? They buy and sell stocks. Can you buy and sell stock? Yes, no doubt. It is as easy as going to a grocery store and buy pineapples.

The argument about them having (insider) knowledge and time to spend on analysis so they choose the right stocks to invest in and thus they are far superior to you also won’t hold water. If the funds’ managers were so far superior to you how come they always fail to beat the S&P 500? Even today, in the extreme bull market those mutual funds average little over 8% annual return!

I was lucky. My own 401k made 15.09% return in 2016. And it was because I spent some time and out of the poor choices we have in the plan I could choose high dividend and distribution paying funds which were then reinvested and thus generating more income. Yet it wasn’t enough to keep the pace and outperform the stock market in the previous and following years.

Here are a few examples:

| Year | 401k | S&P 500 |

| 2014 | 11.18% | 13.69% |

| 2015 | -4.39% | 1.38% |

| 2016 | 15.09% | 11.96% |

| 2017 | 1.92% | 5.94% |

Even with the recent Trump rally my 401k wasn’t able to beat the market! Still not convinced that you do not need those managers and you could learn on your own and get better results?

Then watch this must see video:

· Mutual funds offer far greater diversification which will protect you

I have heard this among people so many times arguing with me that the funds are the best choice for people who do not have enough time to pick individual stocks and money to purchase thousands of them so they can stay protected from falling stocks.

This is the biggest myth and misunderstanding about diversification I have read and heard so far.

At some point diversification can protect you against a fall of one or two stocks in your portfolio. But it will not protect you against systemic risk.

What is systemic risk? It is a risk of the whole system. As was shown in the video above. People saving in their 401k mutual funds were not protected against a fall of all stocks. The 401k will not protect you against a fall of the entire market. If the stock market is in crash or strong bear market, everything goes down. And by everything I mean everything. There is no hideout. In 2008 stocks went down, treasuries went down, gold went down, everything went down.

And how would you protect your 401k? How many of the plans allow you to move in 100% cash? I know none. You can choose a cash equivalent mutual fund but you know what? They went down too!

You do not need thousands of stocks in your portfolio to get protected against a fall of a few bad stocks. My ROTH IRA portfolio has about 15 stocks. Two stocks lost 99% of their value (my risky oil play). Yet my portfolio is in positive territory. Yes it could be in a lot better shape with those two stocks not bankrupting. But my goal is not the value of the portfolio but income it provides.

And if everything goes down during a crisis or sell off, then it doesn’t matter whether you have 15 companies or ten thousands of them in your portfolio.

· You need to save more than one million dollars to retire comfortably

This advice I keep seeing online is the one most ridiculous one which drives me constantly crazy every time I see it. It basically tells you to give tons of money to the 401k managers which constantly fail to beat the market for 30 or more years and you have absolutely no guarantee that you will have that money when you will need them.

And when they fail to deliver, they will tell you that you haven’t saved enough.

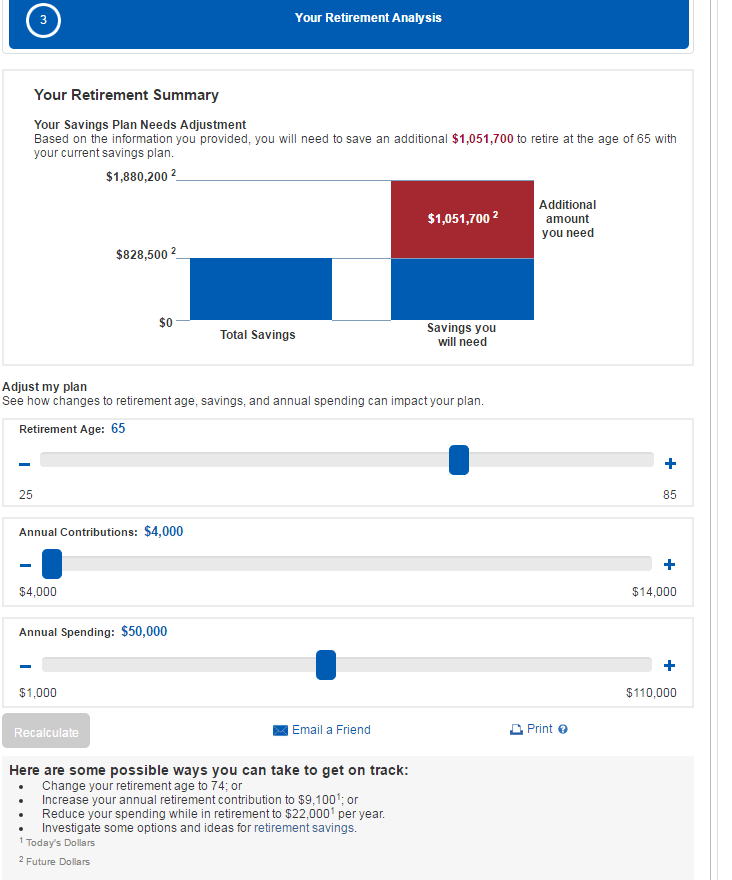

I played with a few calculators online. All of them came up with the same result. All of them showed me that I will never be able to save enough for retirement because I needed $1.8 million of dollars to have saved which I failed to save.

I assumed the following situation:

Let’s say you are a young person, just finished college at 27 years of age and got a decent job paying you $55,000 annual income. You plan to retire at 65 of age and you plan on saving 7% of your income.

Seven per cent of your income is not small money. If you plan on starting a family, saving for a house, or car, $4,000 annual contribution to your 401k is significant shortfall to your family budget.

But let’s say you manage to easily live without it.

Yet, saving 7% out of your annual income is not enough!

|

|

In order to be able to keep up with your retirement goals, you will have to save 19% of your salary every year! At some point in the future when you save enough and your salary starts rising, you might be able to slowly reduce your contributions.

But can you see the ridiculousness of this endeavor?

From your bi-weekly paycheck of $1,798 dollars after taxes you will be sending $400 dollars to your 401k. You will take home $1,390 every two weeks.

Are you comfortable saving this amount of money for the next 35 years not knowing what the future brings? What would happen if you lose job and you will not be able to contribute for a year? You fail your savings! What if you will need medical expenses? A new house for your family?

What if next crisis strikes just 5 years or even two years before your retirement and your 401k account will lose 50% of your savings?

· It’s tax deferred! They say…

Another big myth about 401k is that it is tax deferred and that it will grow tax free and that when you need the money you will pay taxes then at a lower rate.

Seriously?

Are you really convinced that at your retirement, when you will no longer have deductions for kids, mortgage, tax credits of all sorts, which now are helping you to pay taxes in 15% bracket will stay 15% 30 years later? And are you convinced that the government will not increase taxes in the next 30 years so they have enough to pay for all the government entitlements and budget expenses?

Taxes increased by 14% in the last 10 years. In 2007 the limit for 15% inflation adjusted bracket was $15,650 for married filled jointly. Today, it is $17,850.

So what makes you think that you will pay less taxes when you will be withdrawing your saving (if there are any left)?

· The solution? Income!

Yes. Instead of hoarding cash in my 401k account with a sloppy future, sitting there doing nothing, but generating fees for my 401k manager who doesn’t do anything more than what I can do for myself I decided to take a different path.

I decided to use that money to start my own business and make sure that it will generate money after I no longer will be able to do so for myself.

Don’t you think that if you are able to hoard one million dollars that you can use that money for something better than feeding the financial parasites abusing you and your money?

I think I can do better with my future million dollars. And you can do too. You can choose from a few different paths.

You can choose to invest into dividend growth stocks and make sure they keep paying you forever even when you no longer works.

Or like me, you can choose to learn how to trade (stocks, options, futures, or Forex) and make your million generate money for you.

That’s why I started my own trading business, learned how to trade options, and save money into my business rather than 401k. And after about 5 years of learning and mistakes, my business is picking up and starts generating nice cash flow. Not yet enough to retire but getting close.

Uhh…you failed to mention company match. If you are getting a 3-4% match, that is free money…

That “free money” will be ~ $84 bi-weekly @ 4% match.

Tell me, is it still all worth $84 every two weeks to offset all negatives of the 401k?

It may look nice when you are just starting your 401k, but once you save and invest 30 thousand dollars or more, this “free money” will never be able to offset benefits of the dividends. Once you will be able to buy 1000 shares of the dividend stocks, with initial 3% dividend yield, dividend growth 3%, then after 10 years your YOC will be almost 6% and dividend income $158/mo which matches the “free money”. And imagine what I can do with the money when trading options and making 10% monthly (which is what I currently make)!

On top of this, if you compare your own built dividend portfolio vs. 401k at the end of the savings period how your withdrawals would look like?

– with my own dividend portfolio I will be withdrawing dividends and I will not need to sell a single stock (my current dividend portfolio is currently yielding 5% p.a. at 9.44% growth; if I buy 1000 shares at 36 a share today, my dividend income 35 years later will be $1,519,258.00 per year in today’s dollars or $126,604 monthly and unless taxes rules change they will be taxed as qualified dividends at 15% tax rate). In this case, you do not have to touch your stocks and do not have to care what their value is. All you care is that they continue paying and increasing the dividend.

– with 401k, at the end of the savings in order to get income and withdraw cash you will have to sell mutual funds. They do not generate any cash which you will be able to take out. You will have to sell. And what if there will be a financial crisis and you will have to sell when everybody is panicking? And even if you will be selling on top of the bull market, your withdrawal will be taxed as an ordinary income. And good luck getting below 25% bracket with no exemptions available.

Are you still convinced it is worth the “free money” of $84 bi-weekly?

For this initial insignificant boost of “free money” I am not going to block my savings for 30 or more years when I can achieve more than that several times. And everybody can do the same. Investing into dividend stocks is not difficult and not a rocket science.

(All my calculations above were based on a one time investment of 1000 shares at $36 a share, initial dividend yield 3%, and dividend growth 3%. I acknowledge that in the first few years the investing dynamic may not be better than 401k or as shown in my calculations since a young person starting his/her savings will not be able to come up with $36,000 dollars immediately and with a savings rate of $800 monthly it would take 4 years to save that money, but after that and with added contributions, the savings and income from the portfolio will exceeds mediocre benefits of 401k).

Hope this helps to show flaws of luring people into 401k by providing “free money” which actually are not free at all. In the end, you will pay for that free money dearly!

Well, yes imo. In my 401k we have great vanguard index funds and that 4% over the course of a year is almost 5k. That’s not insignificant.

What I do agree with you on is investing in dividend stocks outside the 401k, which is what I do. But I disagree that passing up a free 5k a year is smart. Even in less than ideal investments, it’s still worth it.

But everyone’s situation is different.

I still maintain that it is not worth it. There are other implications such as taxes and withdrawals methods which makes the lure of “free money” worthless. According to your information your annual salary is around $125,000 dollars. Do your math and you will see that whatever you contribute to the worthless 401k can do a lot better elsewhere and that $5,000 free money annually will not offset the disadvantages. Believe me, you can really make more with your contributions than staffing them into a 401k plan.

I wrote another post trying to describe why it still isn’t worth it. It will be published tomorrow morning.

But I agree, as you said, everyone is different and there will be people who will continue believing in 401k as the best choice and decide ignoring the fact that it is expensive and and providing mediocre returns. However, I laid down my reasons for not adding a single penny into my own 401k. All I regret is I haven’t realized this earlier and contributed so much money in it in the past. But, no one is perfect and we learn as we go.

I just hope other savvy investors can see what I see and adopt it and stop wasting their own money. If not, I am fine with it too. :)

Thanks for stopping by.