Although the markets are undecided in the trend, which seems to be slowing down, some stocks continued with sell off today. I am not watching all stocks, but some, mainly dividend paying stocks. And these are under pressure. My almost entire watch list is in red.

Some stocks are retreating slowly in small amounts, some have substantial declines. And those are now worth to consider adding them.

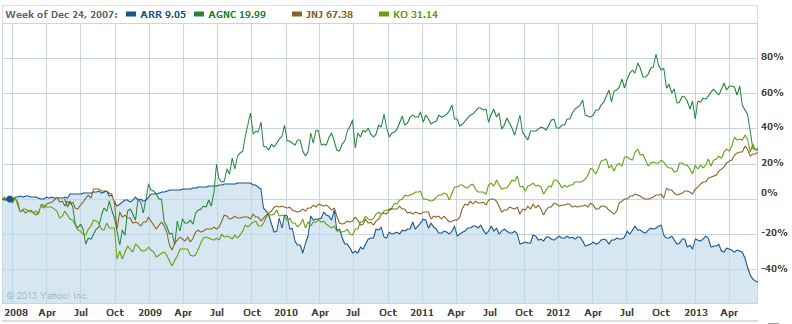

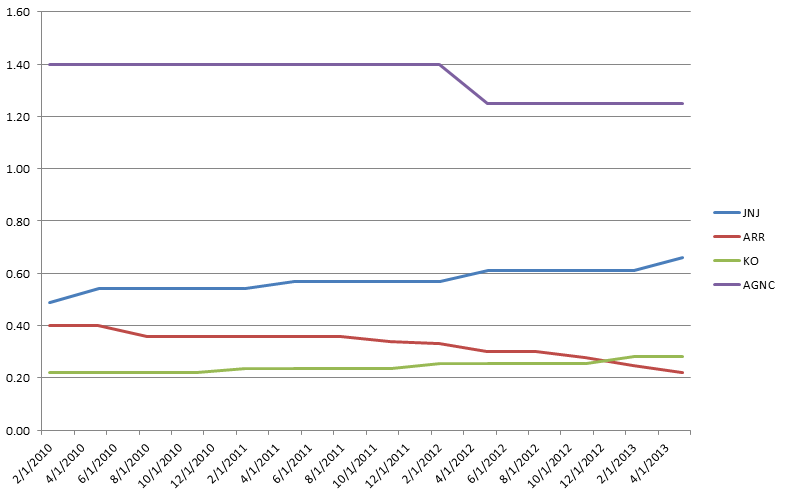

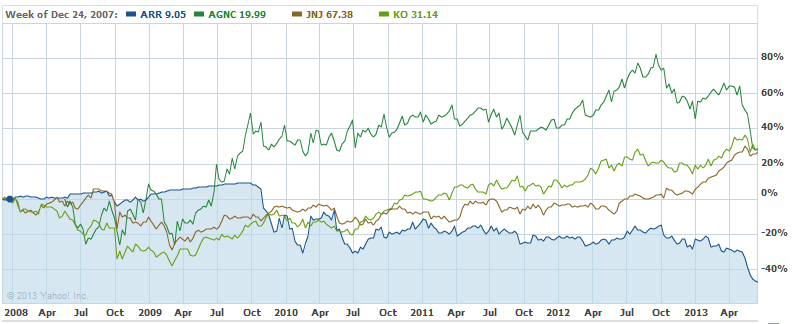

American Capital Agency (AGNC)

A real estate investment trust (REIT). The Company earns income primarily from investing on a leveraged basis in agency mortgage-backed securities. These investments consist of residential mortgage pass-through securities and collateralized mortgage obligations (CMOs) for which the principal and interest payments are guaranteed by government-sponsored entities, such as the Federal National Mortgage Association (Fannie Mae) and the Federal Home Loan Mortgage Corporation (Freddie Mac), or by a United States Government agency, such as the Government National Mortgage Association (Ginnie Mae) (collectively, GSEs). It may also invest in agency debenture securities issued by Freddie Mac, Fannie Mae or the Federal Home Loan Bank (FHLB). The Company is managed by American Capital AGNC Management, LLC, which is an affiliate of American Capital, Ltd. (Source: Thomson Reuters)

Dividend Yield: 18.80%

5 yr. Dividend Avg. Growth: 0.00%

Consecutive Div. Increases: 0 years

Gross Margin: –

Cash Flow: 852M

Cash per share: –

Dividend Rate: 5.00

The Coca-Cola (KO)

The Coca-Cola Company, incorporated on September 5, 1919, is a beverage company. The Company owns or licenses and markets more than 500 nonalcoholic beverage brands, primarily sparkling beverages but also a variety of still beverages, such as waters, enhanced waters, juices and juice drinks, ready-to-drink teas and coffees, and energy and sports drinks. It owns and markets a range of nonalcoholic sparkling beverage brands, which includes Coca-Cola, Diet Coke, Fanta and Sprite. The Company’s segments include Eurasia and Africa, Europe, Latin America, North America, Pacific, Bottling Investments and Corporate. In September 2012, it acquired approximately 50% equity in Aujan Industries’ beverage business. In January 2013, Sacramento Coca-Cola Bottling Company announced that it had been acquired by the Company. Effective February 22, 2013, Coca-Cola Co acquired interest in Fresh Trading Ltd. Effective February 22, 2013, Coca-Cola Co acquired interest in Fresh Trading Ltd. (Source: Thomson Reuters)

Dividend Yield: 2.60%

5 yr. Dividend Avg. Growth: 8.35%

Consecutive Div. Increases: 50 years

Gross Margin: 64.5%

Cash Flow: 1,243M

Cash per share: 2.06

Dividend Rate: 1.12

Realty Income (O)

Realty Income Corporation (Realty Income) is an equity real estate investment trust (REIT). The Company is engaged in acquiring and owning freestanding retail and other properties that generate rental revenue under long-term lease agreements (primarily 10 to 20 years). The Company has in-house acquisition, leasing, legal, credit research, real estate research, portfolio management and capital markets. At December 31, 2011, it owned a diversified portfolio of 2,634 properties with an occupancy rate of 96.7%, or 2,547 properties leased and only 87 properties available for lease. It leased properties to 136 different retail and other commercial enterprises doing business in 38 separate industries. It properties are located in 49 states, with over 27.3 million square feet of leasable space, and with an average leasable space per property of approximately 10,400 square feet. In January 2013, it acquired American Realty Capital Trust. (Source: Thomson Reuters)

Dividend Yield: 4.20%

5 yr. Dividend Avg. Growth: 3.89%

Consecutive Div. Increases: 15 years

Gross Margin: –

Cash Flow: 149M

Cash per share: –

Dividend Rate: 2.17

PPL (PPL)

PPL Corporation (PPL) is an energy and utility holding company. The Company operates in four segments: Kentucky Regulated, U.K. Regulated, Pennsylvania Regulated and Supply. Through its subsidiaries, PPL generates electricity from power plants in the northeastern, northwestern and southeastern United States; markets wholesale or retail energy primarily in the northeastern and northwestern portions of the United States; delivers electricity to customers in Pennsylvania, Kentucky, Virginia, Tennessee and the United Kingdom, and natural gas to customers in Kentucky. As of December 31, 2012, the Company’s subsidiaries were PPL Energy Supply, LLC (PPL Energy Supply), PPL Electric Utilities Corporation (PPL Electric), LG&E and KU Energy LLC (LKE), PPL Global, LLC (PPL Global), PPL EnergyPlus LLC (PPL EnergyPlus), PPL Generation LLC (PPL Generation), Louisville Gas and Electric Company (LG&E) and Kentucky Utilities Company (KU). (Source: Thomson Reuters)

Dividend Yield: 4.80%

5 yr. Dividend Avg. Growth: 3.01%

Consecutive Div. Increases: 13 years

Gross Margin: 41.7%

Cash Flow: 2,713M

Cash per share: 1.44

Dividend Rate: 1.47

AT&T (T)

AT&T Inc. (AT&T) is a holding company. AT&T is a provider of telecommunications services in the United States and worldwide. Services offered include wireless communications, local exchange services and long-distance services. AT&T operates in four segments: Wireless, Wireline, Advertising Solutions and Other. Its Wireless subsidiaries provide both wireless voice and data communications services across the United States, and through roaming agreements, in a substantial number of foreign countries. Wireline subsidiaries provide primarily landline voice and data communication services, AT&T U-verse TV, high-speed broadband and voice services (U-verse) and managed networking to business customers. AT&T’s Other segment includes customer information services (operator services) and corporate and other operations. On May 8, 2012, AT&T sold its Advertising Solutions segment. (Source: Thomson Reuters)

Dividend Yield: 5.00%

5 yr. Dividend Avg. Growth: 3.36%

Consecutive Div. Increases: 8 years

Gross Margin: 56.8%

Cash Flow: 29,429M

Cash per share: 0.72

Dividend Rate: 1.80

There are definitely other companies available which are recently declining, but the above companies I have in my portfolio (except Coca-Cola) and my rules are now to accumulate instead of buying new companies into my portfolio. I described my rules in this post how many companies I want to hold in my portfolio based on the size of the portfolio. I am not strictly following that rule, however, I want to be accumulating more rather than adding new companies.

Happy Trading!

We all want to hear your opinion on the article above:

6 Comments |

If you have time to spare and browse thru the message board about this stock, you get the impression that this stock has a lot of value and you know absolutely nothing about investing into mREITs. The stock trades at $4.85 a share and its estimated book value is at $5.50 a share. So many will argue with you that if you have bought below $5 a share you were buying at a great discount and you cannot lose. On top of that you would receive a hefty dividend every month. What can go wrong, right?

If you have time to spare and browse thru the message board about this stock, you get the impression that this stock has a lot of value and you know absolutely nothing about investing into mREITs. The stock trades at $4.85 a share and its estimated book value is at $5.50 a share. So many will argue with you that if you have bought below $5 a share you were buying at a great discount and you cannot lose. On top of that you would receive a hefty dividend every month. What can go wrong, right?

{kind=link}

{kind=link}

{kind=link}

Recent Comments