In my previous article I advocated for keeping cash in my account for potential purchases when opportunities show up.

The principle I was looking at is save cash in the account during market upward run, minimize buying, only when a stock you are interested in shows you an excellent buying opportunity such as a dip (make sure the dip is not caused by a fundamental problem, but by big investors pushing the stock down to shake off retail investors, for example) or the stock currently trading at the support level, breaking from the base etc,.

When the market starts falling, then that will be my time to start looking for stocks on sale and use accumulated cash for buying. But do not use all of your cash all at once. Split your purchases in smaller lots. I use $800 or purchase lot.

Market direction

Looking at the market, we can still see a positive trend, but currently the market is extremely overbought.

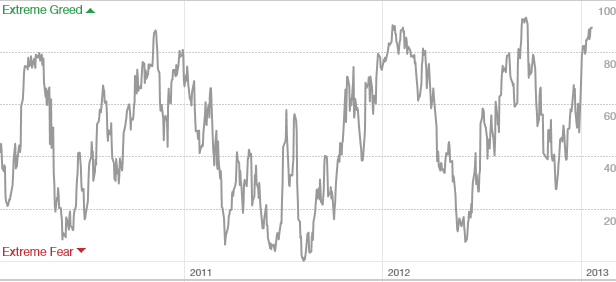

I mentioned in my previous article that I like to use Fear & Greed indicator (see above) to get a quick sense of where the market is. You can find that chart at Money CNN website. Today, the chart indicates “Extreme Greed” and the value at 90, which is the same value as one year ago. And the similar value as two years ago.

If we assume that the market moves in cycles, we may expect a repetition in future. The future may look like the one at the beginning of 2012 with a slightly prolonged period of time hanging at those elevated levels, or in the middle of 2012 with sharper correction. The fact is, the market will not stay at these levels for ever and will correct or pull back.

The pullback may look like the end of 2010, relatively shallow one, but it will be there. It will happen.

Well, let’s take a look at VIX (volatility index) which I also look at when trying to find out what’s going on with the overall market.

The VIX index is currently at 12.43 level. When was the last time you saw the index that low?

Well, I save your time and tell you. In 2006 – 2007 period before the market crash in 2008 (by that, I do not want to imply that the market will crash). Look at the oscillators. Both, the Ultimate Oscillator and MACD are in oversold territory (but MACD is not indicating reversal yet).

However, This doesn’t mean, that the market will fail tomorrow and start falling like a rock. It looks like there is still a lot of capital flowing from bonds to stocks and we still may see a long period of market going up and up and up like without the end. When you take a look at intraday charts, you can see that the investors are picking up every dip which occurs and buying stocks. That indicates there is still a lot of money.

What to do?

Do you want to chase this market? All stocks I wanted to buy were following the overall market’s trend and they are overextended.

NGLS – dramatic break thru above 200 day MA. Great sign, but extended almost 10% above 50 day MA. The stock may correct this extended run back to 50 day and continue back up. Indicators are in overbought territory and slowing down.

PSEC – steady uptrend without a rest. Indicators slowing down dramatically, MACD showing a crossover and moving into negative territory. Ultimate Oscillator is already negative (but still close to overbought and heading down). Stock extended 6% above 50 day MA.

FGP – a parabolic run up, hitting upper Bollinger Band, reaching November 2012 major pivot point (top) or resistance, we may expect the stock to bounce off of it down before it breaks up. Ultimate Oscillator in overbought, MACD just crossed into a positive territory as well as Chaikin Money Flow indicator (which I also use). So this stock doesn’t look that bad, but signals are mixed to make a decision.

Do you want to start shorting the market (if it is your trading philosophy)? I wouldn’t do it either, although there is a growing number of traders who are moving to the bear side of the market out there.

However, I am still saving cash, because I believe, based on what I see on the charts (and I like it, because I can see nice capital gains), that this market is due for correction. It can be a small one, just down to 1450 level (SPX) or 1430 or even 1400. And that will be a great opportunity, to add more shares to my portfolio.

Why buying now, when the prices are high, when I can be comfortably saving cash (which I have to do anyway) and as soon as the market starts correcting start picking up those sweet cherries on the top of the cake instead of buying now and when the correction begins ride it and sitting on losing stocks for who knows how long. And honestly, I hate seeing my account with too many red numbers in it.

Happy Trading!

We all want to hear your opinion on the article above:

6 Comments |

I no longer believe in mutual funds. Earlier I thought they were a great investment vehicle, because they can provide diversification. But is it really such a significant trait of the funds that it can beat mutual funds flaws?

I no longer believe in mutual funds. Earlier I thought they were a great investment vehicle, because they can provide diversification. But is it really such a significant trait of the funds that it can beat mutual funds flaws?

Recent Comments