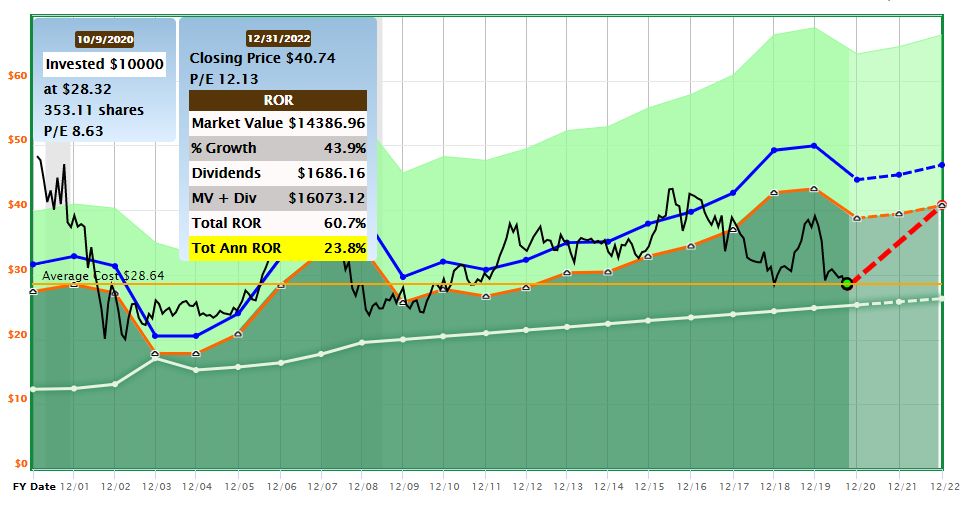

The stock market was forming a cup and handle formation, but yesterday, this pattern failed.

If we were to continue the pattern, we were supposed to continue higher as indicated in the picture below:

Since this pattern failed, what is ahead of us now?

We can see or identify two other possible patterns:

1) A double top formed and we may see the price to go down to 200 DMA

The double tops are rare and do not occur very often (no matter how much others on Facebook tell you otherwise). And even if they do occur, experienced chartists say that they are not very reliable patterns. Why? One reason is that it is very typical for the price to get some harsh time at the top resistance and it may take a few attempts for the market to break that resistance. Thus the price stalls once or twice, sometimes three or four times before it breaks up. Short term, you may identify it as an intermediate movement stop with a small pullback but definitely not a major trend reversal. You may look at the double top as a consolidation pattern rather than a major reversal one. Most of the time. Sometimes, it will not work as consolidation, and the price crashes. If this is the case today, we may see some violent downturn down to the 200-day moving average:

Given the election is in a week, after that, we may expect stimulus to pass, the market may recover from this pre-election weakness and continue higher. If that is the case (and I think it is), then the second emerging possible patter is the one in play:

2) An upward sloping triangle

This pattern seems more probable but we will have to wait for the resolution. If this is really in play, we are not out of the woods yet, the market may continue in a zig-zag move for sometime before we find out whether we break up, or down.

|

We all want to hear your opinion on the article above: No Comments |

Recent Comments