Account Net-Liq: $7,735.95

SPX value: 3,380.35

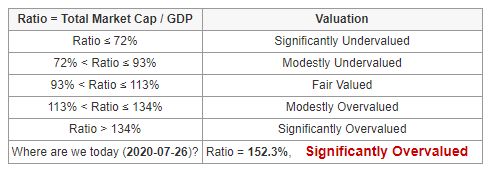

Shiller PE: 31.27

This is an entry I wrote into my Trading Journal yesterday about the market behavior:

Are we going to see a correction?

Account Net-Liq: $7,815.02

SPX value: 3,333.69

Shiller PE: 30.83

After a relentless rally, the markets suddenly sold off at the end of today’s session. Of course, the media are telling us that it was because of some new optimism of the vaccine and now because of some pessimism over that same vaccine which everyone was so optimistic just the day before. But who cares. We needed the market to ease a bit. So this dip is welcome. Unless it turns into something else, it is just a dip. And as such, buy the dip. And I think, we are at the beginning of a long term bull market (well, I would say next 5 years) and economic expansion. So, if there is a dip on the road to that economic expansion, buy that dip. And be prepared that the dip may be up to 5% deep, and it will be a very common thing.

I had some other members who follow my market reviews (for which I take no responsibility and no guarantee of it being correct – remember, I totally suck in technical analysis and I do this to learn it. And the best way to learn it is doing it.) asking me if I expect this selloff to continue. My response was that no, I didn’t expect it to continue. I thought it was just a blip and a small dip.

I also had some other members asking me if I think a second crash is coming. Again. my response is – no, I do not expect it. I do not see any fundamentals for it to happen:

- There are still tons of cash aside sitting in savings accounts making close to none interest. These monies need to start shifting from the savings accounts to the market. It has not yet started happening.

- People are still too pessimistic and out of the market. If you look at AAII (American Association of Individual Investors) sentiment poll, over 40% of investors are bearish. This is unprecedentedly high number last seen in 2008 and we have not had any similar crisis like in 2008. Today’s crisis is artificial and will not last forever. It is not a systemic crisis that would turn this bull into a long term bear.

- The market is pricing a LESS BAD economic outcome. No one, even the worst pessimist can expect the economy to be down forever. The average recovery takes 1 to 3 years. But this time is valid in case there was systemic damage. The COVID is not systemic. This was an artificial stop and it will pass. Businesses are opening more and more, and the economy will recover no matter what you think about the valuations and economic activities in the US.

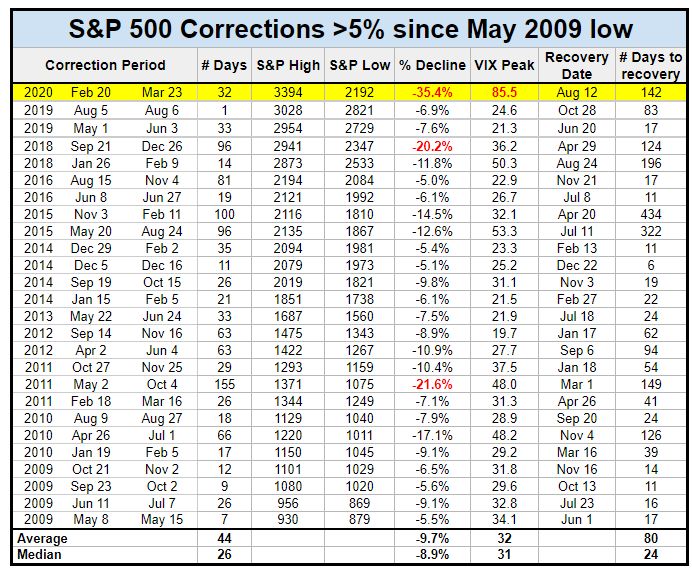

- Don’t forget the FED. I believe, FED is the main reason why all the good ole valuation metrics no longer work. If you look at the market PE (or Schiller PE) and decide to invest when the stocks become cheap based on these metrics, then I have bad news for you – you will never invest, thanks to FED’s involvement and artificial inflation. Do you think the market will ever correct from this inflation? Well, yes, maybe, one day it may. But we recently just went through a 40% decline. A 40% decline is a serious correction. If you think otherwise, you need to study the previous market history. A 40% decline doesn’t happen very often. And, you know… FED, when such a decline happens, FED is always here for you to bail you out (well, if you are invested instead of sitting aside and waiting for valuations). Another thing about valuations is that the last one favorable one happened 20 years ago. Since then, the market always traded at a premium. And, even Ben Graham admitted that PE has an expanding feature built-in, so during his times, the average market PE was 20, but he recommended using 25 because of the PE expansion. Today, the average PE is 28, but we constantly trade around 20 – 31. Last time, when the market dropped below 28 was… you guessed it – in 2008. And, do you have time to wait for another 10 to 15 years for the PE to drop below 28? I don’t!

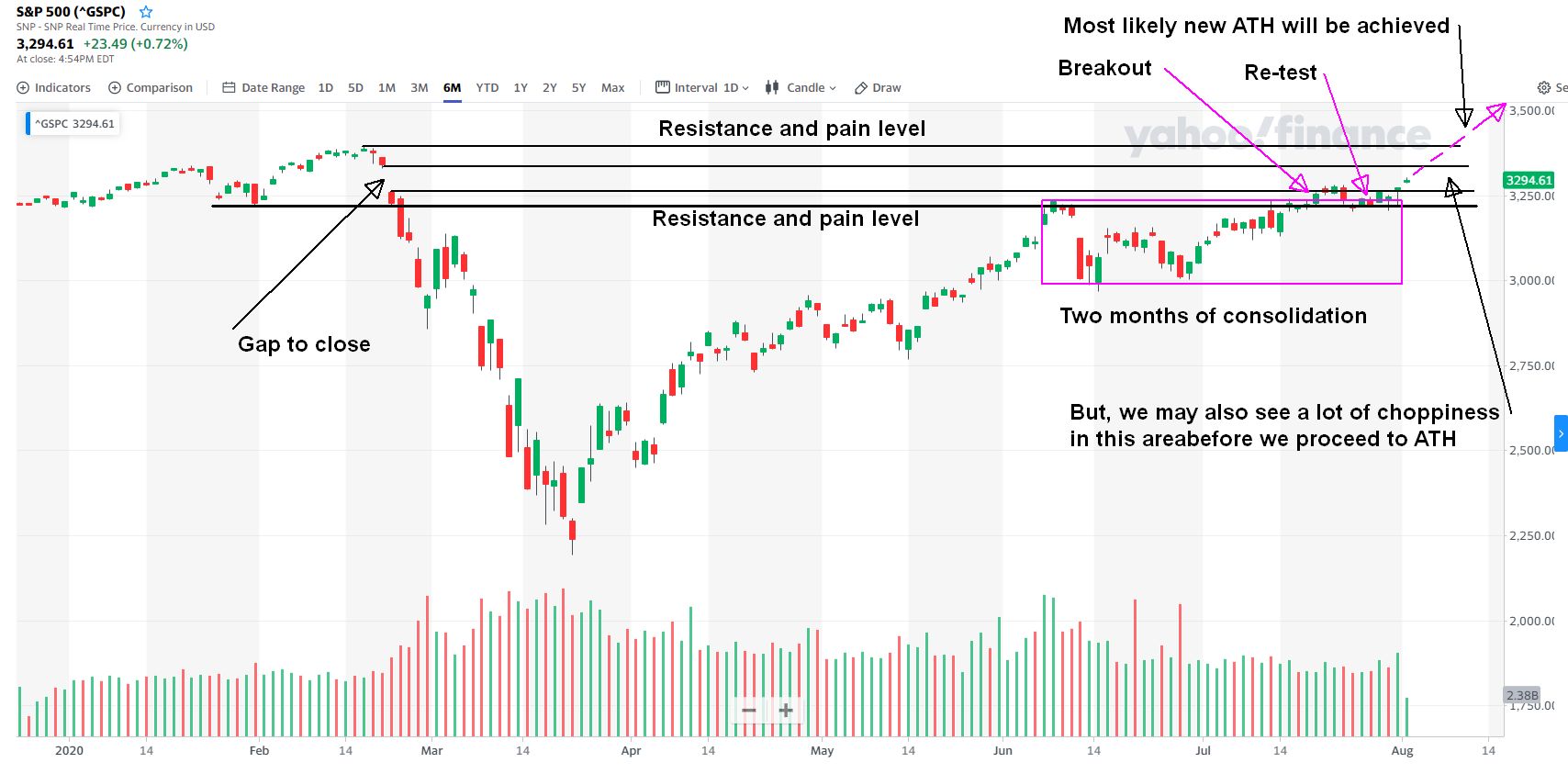

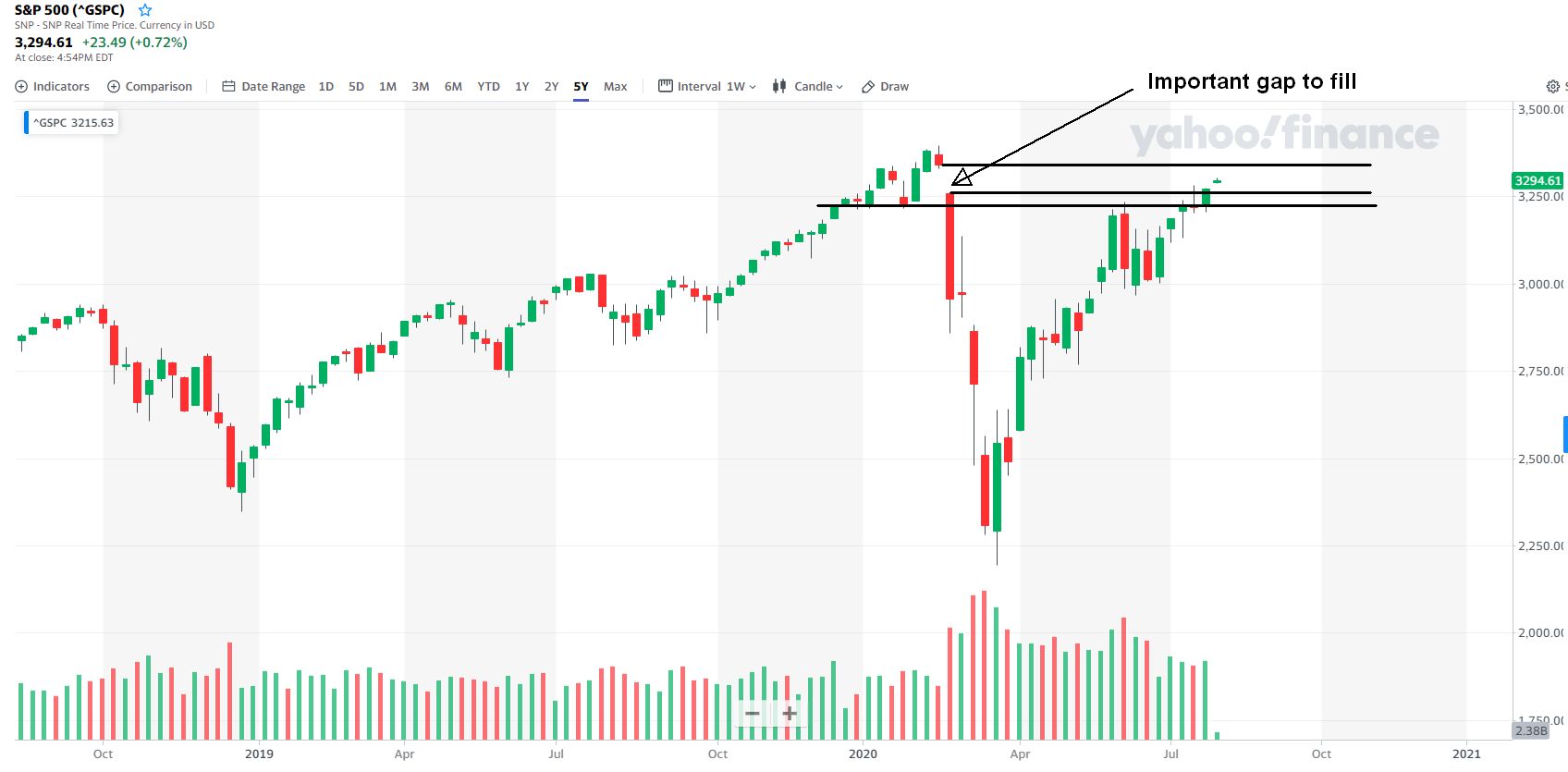

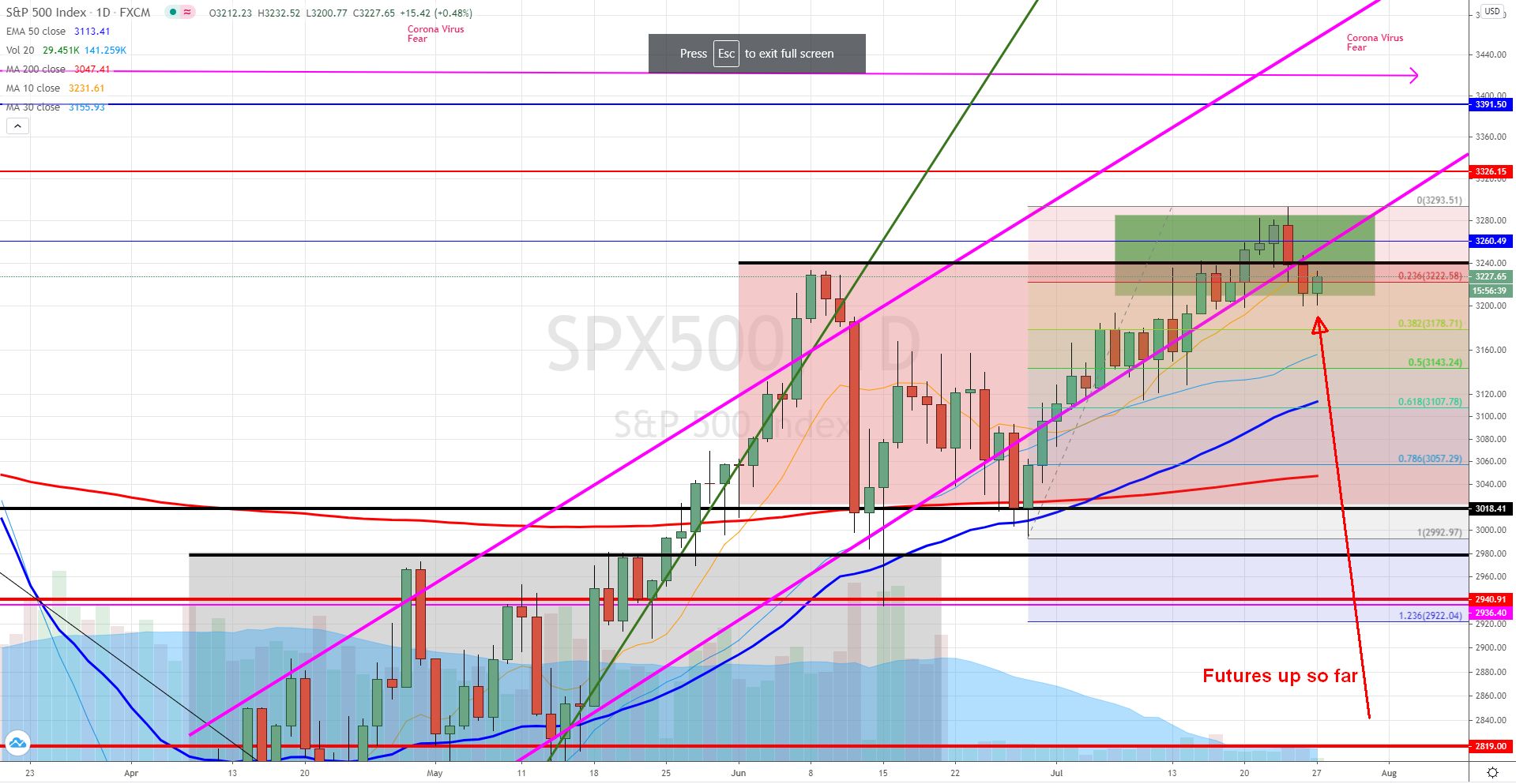

And today, the market rallied hard and not only erased all the losses from yesterday but also added more gains. We are almost where we were before the COVID crisis. The previous ATH was at 3394, today, we have reached 3388.62 and returned back into the channel. Until this trend breaks, do not expect any change in direction. All previous breaks down were in fact just dips. We had no confirmation from those dips and the market was immediately bought back and went up again. Thus my expectation is – up again.

This is also confirmed by big market participants who are positioning themselves for a big economic expansion (moving money back to traditional industrial sectors). So, big players do not expect a crash so why should you?

Join us at MeWe to see trades we take.

|

We all want to hear your opinion on the article above: No Comments |

Recent Comments