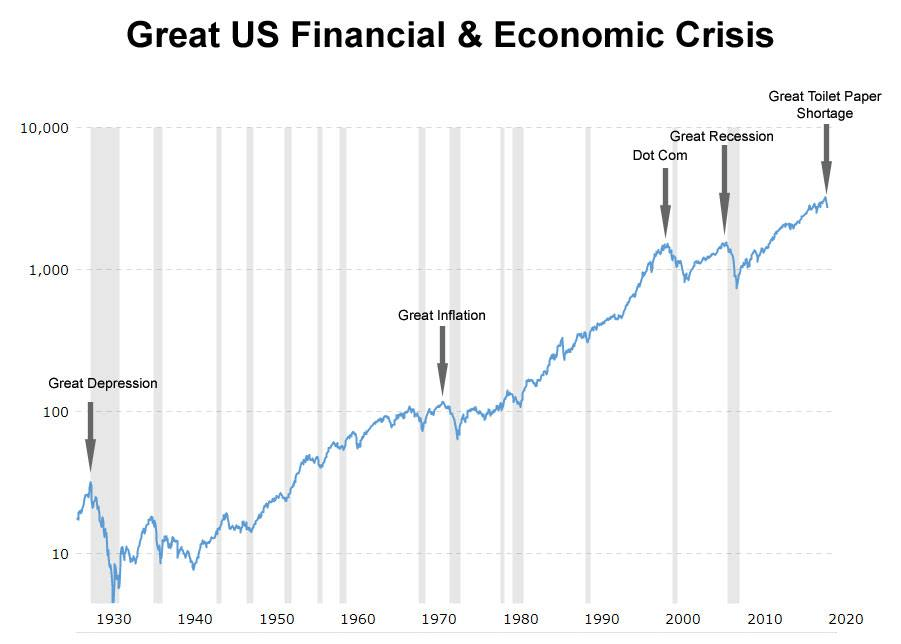

This was hard few weeks on Wall Street with markets flushing out a lot of value over a flue. And yes, I mean it. This is just another version of a flue we know about. Scientists were able to identify the virus genome 10 days after outbreak and worked on a vaccine and solution. All the deaths so far were people of older age and/or those with health problems, pneumonia and compromised immune system. No healthy person died of Coronavirus. One sign can be children. Usually elderly and children are the most risky categories, yet Coronavirus has no impact on children. Only elderly and sick. Yes, you may call me cynical, rude, or any other names you want, but I stand behind this and behind my next claim, that this hysteria and panic is a pure idiocy and self-inflicted pain. Let’s call this market sell off A Great Toilet Paper Shortage!

And so, while we see people going on panic shopping, buying out all the toilet paper, meat, eggs, milk, and other food supplies:

This is an ice cream freezer… half empty. Who the heck is hoarding ice cream?

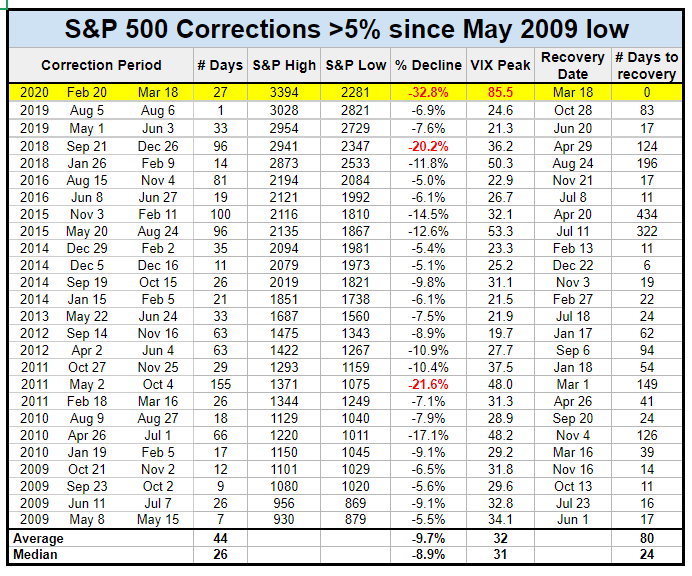

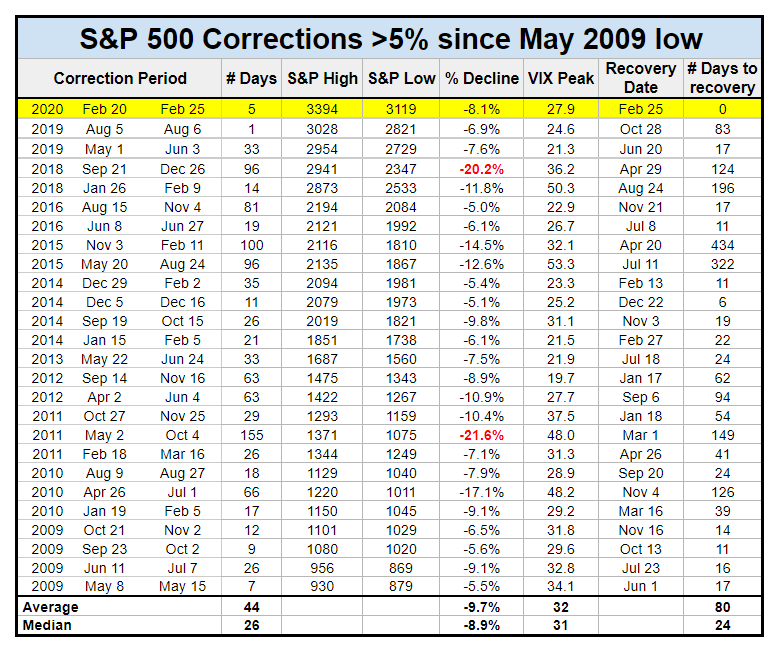

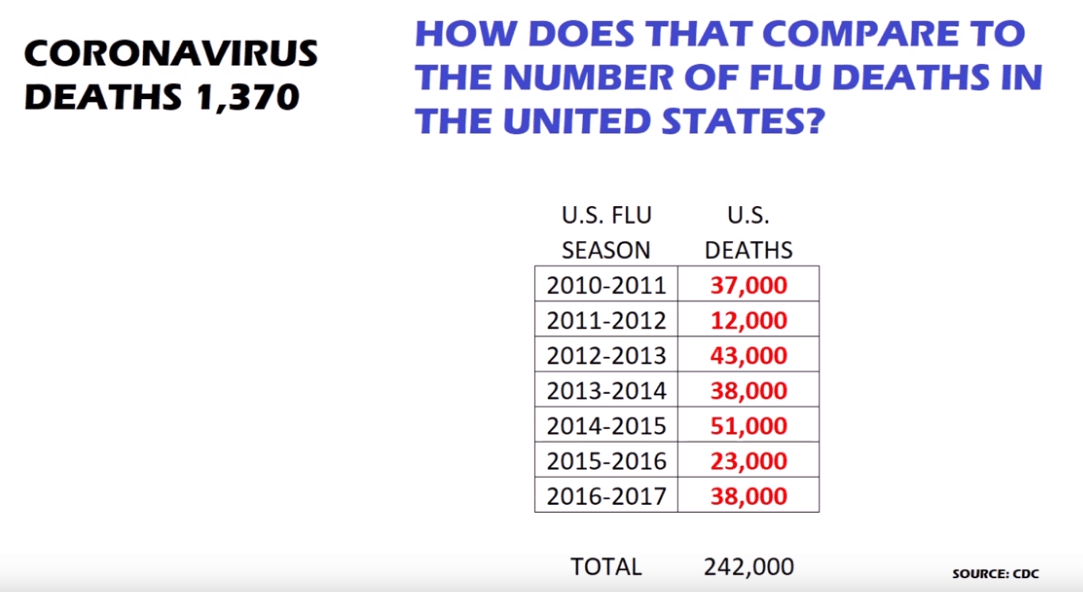

The markets lost over 32% and VIX spiked to 85.5 level. A level not seen even during 2008 crisis. And this is all insane. And this is all a self inflicted pain, self inflicted recession (if we fall into it). Yes, I am not downplaying the virus. I am downplaying the hysteria around it. Every year, just in the US alone, more than 30,000 people die of influenza. Who cares about these people? Who is closing stores, sports events movie theaters, sending employees home over influenza; every year? No one. NO FUCKING ONE!

However, days like those we are currently experiencing are a great opportunity to invest and make nice profits once the markets rebound. And they will rebound.

But, it is also time to protect your capital. That is why we suspended all trading and in fact closed some of our positions.

Although we took a loss on those closed positions and we are sitting on paper losses on our long term open stock position, we look at all this positively. We closed all naked puts for a loss (our trade journal here on FB page hasn’t been updated yet) and took a loss. The reason was to preserve capital and avoid margin calls as these were the positions hurting us the most.

However, when all this mess and panic ends, we may re-enter those positions and re-establish the trades and manage. We will also start new trades.

We keep sitting on our stock positions and in fact keep adding shares as the market keeps falling. We feel that this is a great opportunity. But we also see that the market hasn’t bottomed yet, so we are not buying too much yet. Only a few shares here and there.

Over the course of the few weeks we bought a few shares of SPY, CLX, BIF, XLU, and we plan on adding BA, BAC, PPL, JNJ, and other shares from our watch list. When the panic selling ends, we will also start selling naked puts. What do we mean by “when the panic selling ends”? Once the market stops having these 10% wild swings to both directions then we start selling puts. We are OK with the market still falling or better say drifting to the downside and selling puts, but we do not want to sell puts and see the stock plummeting 10% or 20% in the next two days. We want fairly stable market no matter what direction. And we are getting there.

You may ask why we are not taking advantage of this volatile market and actively trade puts or calls and take advantage of these swings and make tons of money? Look at others in other Facebook groups posting their trading results making thousands of per cents in profits! Well, we no longer trade that way. We may be trading and take trades such as butterflies, or Condors here and there, but we are primarily investors and buy for long time to build a portfolio which will be delivering income long term. And I bet, those people who are boasting great profits today, will stay silent about their losses tomorrow.

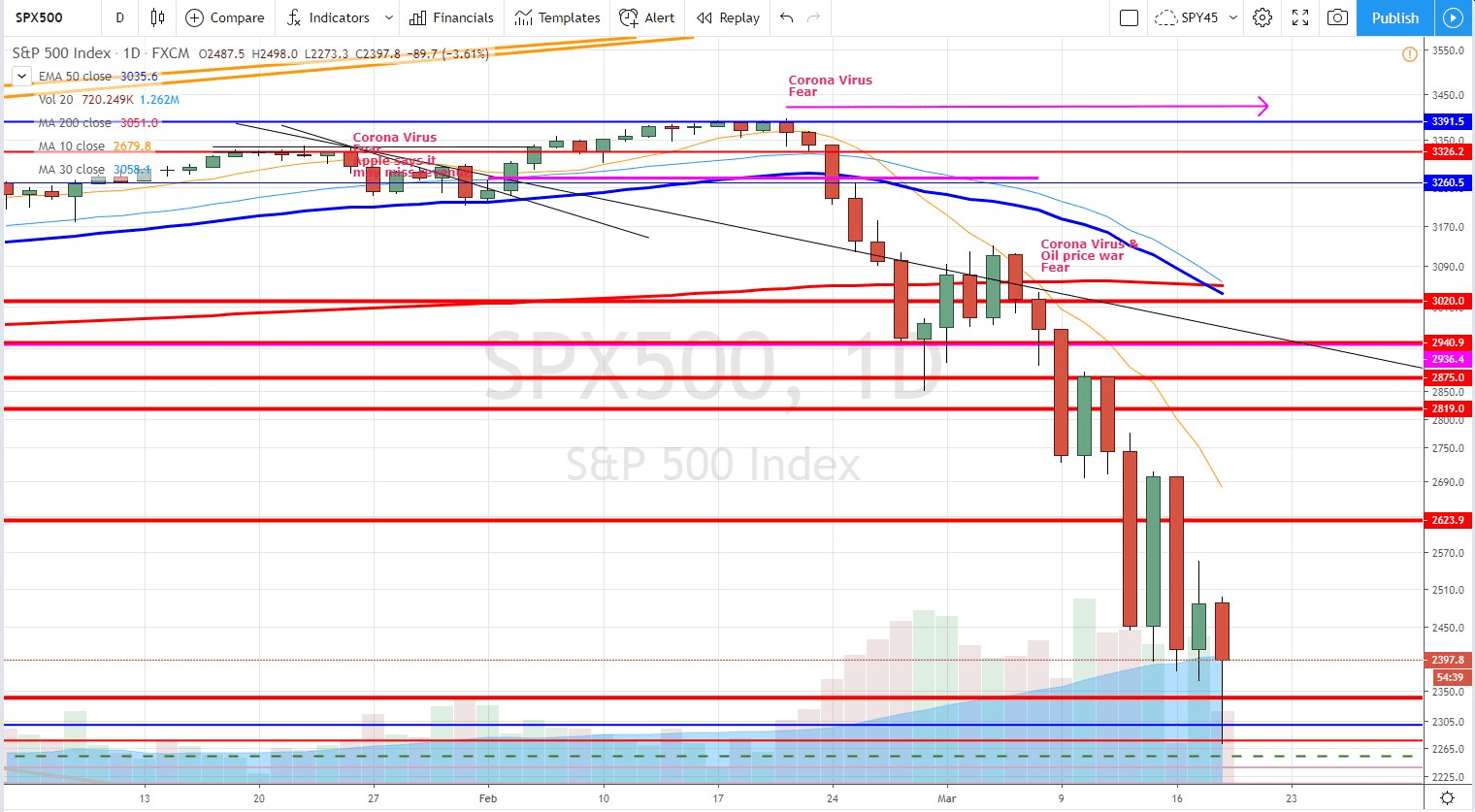

And today, we had another beautiful day at Wall Street… We dropped 9% intraday at some point.

But, there was one difference from other days which may turn positive for the markets. We now have a long shadow candle. That means, buyers were stepping in (although it seems on a very low volume, (but since volume on SPX is derived from futures trading, it still may not be the final volume).

This could be positive for the markets.

Or it can turn out to be a set up for a bear rally to some of the previous levels (I would expect 2750-ish) and then resume of a selloff.

Well, we need to wait to see.

We all want to hear your opinion on the article above:

1 Comment |

Recent Comments