I have followed Keith McCullough, the owner, CEO, and commentator at Hedgeye for some time and for the period of time he was spot on reviewing economic development of the US and its reflection to the stock market.

For a few last years, I think it was years, Keith was bearish on the US economy and the his view at market was reserved at minimum.

He caught my attention by pounding Janet Yellen and FED policy. Hedgeye’s memes that FED has it always wrong were entertaining.

But I considered Keith McCullough to be a permabear.

So I was surprised when his economic and stock market reversed some time ago (about a year ago now) and he presented his bullish view supported by economic data.

Today, Hedgeye came up with yet another article mocking Wall Street and talking heads for once again being on the wrong side of the river.

Enjoy:

Mainstream media and stock market bears have been kicking around this “soft” versus “hard” economic data meme for a while now.

“Soft” data are supposedly measures like Consumer Confidence, which just hit a 16-year high. Meanwhile, “hard” data are releases like Retail Sales, Durable Goods, Capital Expenditure and Jobs Growth which MSM says have been disappointing recently.

Nevermind that Retail Sales recently hit a five-year high, Durable Goods and Capex both accelerated for the month of March and Jobs Growth recently picked up for the first time in 23-months.

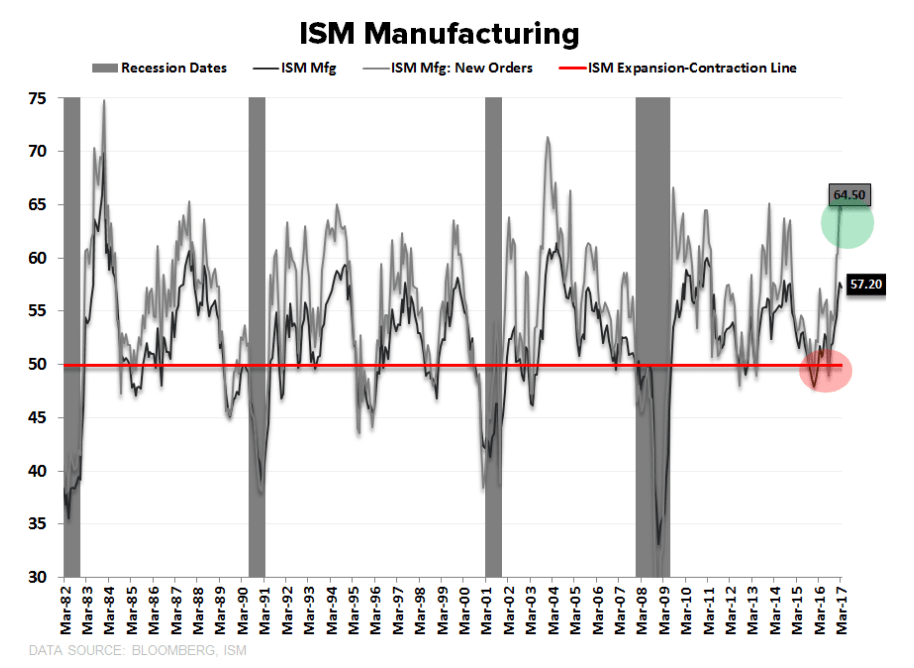

Forget that. The soft data will soften they say. Not a lot of softening of the “soft” data, yet. Today’s ISM Manufacturing data shows the Prices Paid component of the index closing the first quarter of 2017 at a 71-month high of 70.5 on the Index.

The Current Production component dropped below the 60-level while New Orders held just below multi-year highs. Employment is the big callout rising to 58.9 = highest level since June 2011 and Inventory positions continue to improve.

A few notes:

- New Orders are still strong but its hard to expect sustainable ramp from current levels. Middling may be more realistic as commodity/industrial base effect support will be waning and a protracted run >65 in mean reverting, diffusion series is an elusive beast.

- Inventories = custom inventory positions continue to improve as inventory-to-sales ratios continue to improve broadly. In other words, inventories are unlikely to be either an outsized driver or drag on investment nearer-term.

Too bad all these “soft” data experts didn’t call it out when it was softening like it did between first quarter of 2015 all the way to the low for GDP (of 1.3% year-over-year growth) in the second quarter of 2016.

Review the rest of the article at Hedgeye…

Leave a Reply