Strategy

2024 Strategy

In 2023, I developed my trading strategy to increase income from our portfolio. In 2021 and 2022, I started trading options against SPX again. The 2021 year was great, but I ignored cash management. My old bad habit. 2022 was a brutal year, yet we rolled back old trades from 2021 and increased investments. I am happy about it. In 2023, I developed an SPX options strategy called “Crumbs” method. I started trading it in September 2023, and out of 70 trades, the strategy lost only four trades. All the others were winners. You may say that in a bull market, everyone is a genius, and you are right. The strategy may not work well in a bear market either. But I started at the beginning of September, a pullback in the bull market. My old system would fail; this one held.

· Dividend Investing – Asset Accumulation

In 2024, I will continue accumulating dividend stocks. I will focus on dividend growth stocks and add a few high-yield dividend stocks such as REITs, BDCs, and MLPs. They are risky but bring in higher income. The goal is to accumulate 100 shares of those stocks I already own.

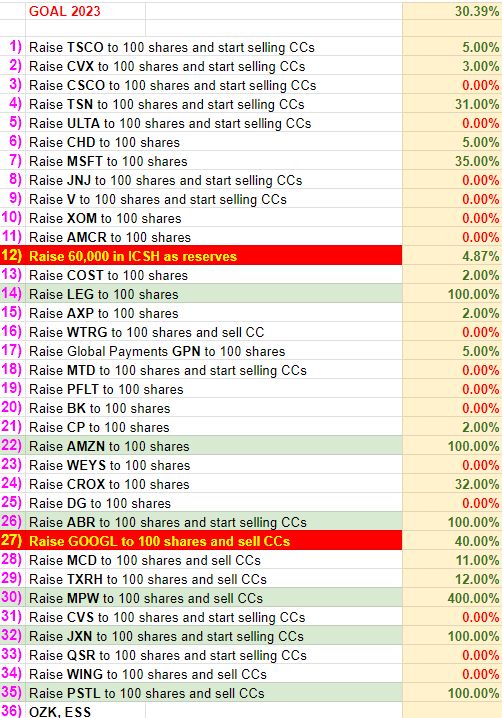

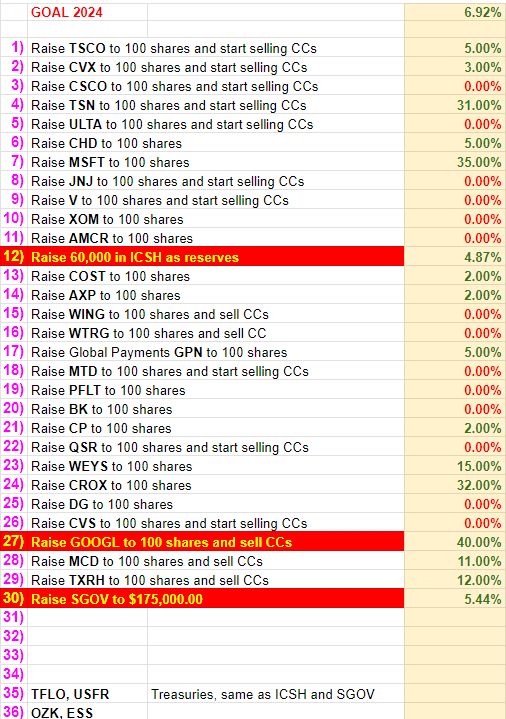

Below are my goals for 2023 and 2024 stock accumulation. The white rows are tasks to be performed, the green highlighted rows are completed tasks, and the red rows are tasks that I am currently focusing on. The focus will change over time, but as of now, my main goal will be accumulating cash in ICSH and SGOV.

· Growth Stocks Accumulation

Besides dividend stocks, I will accumulate growth stocks, too. I neglected them before, but I admit that growth stocks can significantly increase one’s portfolio. However, I will accumulate solid, established companies, no high-fliers or speculative stocks.

· Covered Calls and Strangles

2024, I will keep selling covered calls against dividend and growth stocks. If a covered call gets in the money, I will add naked puts to allow for rolling the calls higher and away in time to avoid having my stocks called away. If an assignment happens, I will repurchase the stock.

· SPX Crumbs Strategy

Last year, I started trading the Crumbs strategy. The process is simple. I will sell primarily Iron Condors against SPX with deltas <5 and 0 to 2 DTE (sometimes 5 DTE if trading over the weekend). With a delta below five on both sides, it is improbable that trade will get busted. Of course, it can happen; anything can happen, but the odds of it happening are lower than with trades that are closer to the money.

The trades are positioned at 2 SD (two standard deviations), and if the market drops by 2 SD, we may expect a bounce the next day, which may save the trade from being busted. The market would have to crash or grow by 1.50% to 2.50% (depending on implied volatility) in a day or two, and that is also less likely in a regular market.

The profit with these trades will be smaller than most traders do. I will only collect $15 – $30 premium per trade. But if I collect this premium every two days (on average), the account can grow very fast. If we have 250 trading days in a year, I will collect $30 per trade. I will be able to bring in approx. $3,750 in premiums per year. But scale the transactions up, and it will grow a lot more.

In bear markets, we can see more significant drops, of course (in 2022, we saw 4% drops in a day), and when that happens, I hope to be either out of the trade (not trading) and if I happen to be in a position that gets busted, I will roll such trade.

So, my exit plan with the Crumbs strategy will be to let each trade expire worthless for a full profit. Alternatively, if the trade gets busted, I will attempt to make two adjustments:

1) Roll the untested spread to create an Iron Fly (if puts get in the money, I will roll calls down to align a short call with a short put, and vice versa).

2) I will close the untested side (short call or short put) to release a buying power (BP) and roll the tested side away in time, and either the same strikes or up or down as needed.

3) I might also widen the spread to reduce the cost of the spread or collect a credit.

Here is our 2023 SPX Crumbs strategy spreadsheet:

· Stocks Crumbs Strategy

I will also trade the Crumbs strategy against stocks. The approach is similar to the SPX except using individual equities.

I will evaluate these stocks monthly and open a new trade to collect at least a $20 premium (after fees). Also, the goal will be to open a 30 DTE trade 20% below the current stock price. With this setup, a stock is unlikely to get busted by 20% in 30 days (if it is an established company). But, again, it still may happen; anything can happen in the market, so don’t get me wrong, this is an invincible strategy. If it happens, I will roll the put away in time, and if possible, to collect credit, I will roll it down. If none will work, let the put assign and buy 100 shares of the stock.

· Futures Crumbs Strategy

At the end of 2023, I tested trading the “Crumbs” strategy against E-minis (/ES Futures). There are two aspects why I liked it. One, Futures can be traded 24/7. Two, this can also substitute for the Stocks Crumbs Strategy. The problem with the stocks was that the Crumbs strategy could be traded against stocks priced at >$100 a share. And many stocks that are priced at $100 – $150 a share have no premium available. So, I would have to trade pricier stocks, like NVDA, COST, MSFT, etc., but these have a hefty margin requirement. If traded the same way, futures will require only about 10% of the stock margin requirement (for example, ABDE stock would require $4,772.80 buying power; Futures would only need ~$400 BP).

If no stock can be traded in a given month, I will use Futures instead.

I will also trade the 45 DTE ladder. That means that I will slowly open trades with 45 DTE until I have a trade on every expiration day. That will require approx. $18,000.00 buying power and it can deliver approx. $1,350.00 premiums every 45 days. But this will be a matter of scaling up the account so that it will be a slow process and not an overnight endeavor.

· Cash and Trades Management and Account Scaling

This part of my trading will require a lot of discipline, which I need to improve, and I tend to overtrade with insufficient money to sustain any losses eventually. So, I will dedicate the entire 2024 to getting my account in order regarding cash and trade management. In my Trade Journals, I created a section which will help visualize my progress.

My new cash management for 2024 is as follows:

1) 50% of the portfolio will be in dividend and growth stocks.

2) 20% of the portfolio will be dedicated to options trading.

3) 30% of the portfolio will be in cash reserves.

Here is my allocation at the beginning of 2024:

As you can see, my allocation is not up to the goal, so 2024 will be dedicated to aligning my portfolio with the plan.

Scaling Options Trading

I am setting a $10,000.00 of the funds to trade the SPX Crumbs trades, but I can open trades using only about 60% of this amount at any given time. Also, each open trade can only risk 5% of the amount. At the beginning of 2024, I violated this goal, so again, in 2024, it will be my task to align the account with this rule.

All proceeds from the SPX Crumbs trading will be parked in the ICSH fund at the end of every month.

Once the savings in the ICSH reach the allocated cash for SPX trading (as of today, $10,000.00), I will scale my options trading up. For example, once I save $12,000, I will raise the allocated amount to $12,000.00. That will increase the number of Iron Condors contracts or widen their spread. Until then, I will only trade the same amount of contracts without increasing the size.

The savings and scaling described above also apply to Stocks Crumbs trades and Futures.

Cash Savings

The next part of my 2024 strategy will be to increase cash savings. For years, I was always fully invested, which proved me wrong. When a bear market hit, I didn’t have enough cash and was forced to close trades at a loss. I also missed great opportunities. For example, I could buy Netflix (NFLX) below $200 a share when investors panicked in 2022. I tried but needed more cash to keep holding the position. Margin calls came, and I had to sell to release BP. Even today, I am pissed at myself for this missed opportunity.

Bear markets are part of this game and will come again. And when they do, I want to be prepared. In 2024, I will save money in the SGOV fund. I will start buying equities only after this goal is achieved.

The tasks above cover my 2024 strategy and goals. Let’s revisit it at the end of 2024 and evaluate it.

Grt read

Very clear information thank you

I’ve read through the pages, but what are your typical parameters for your puts (i’ve seen different deltas and closing %) but i’m unsure if that’s part of your current strategy. Since you’re going ahead and using your credit to buy stocks, I assumed you were letting them expire worthless, but I was just looking for some clarification, thanks.

Moreover, when we start trading options in our challenge account, I will be explaining this process more in detail.

Thank you for your input and question. I have tried to write my rules or metrics when selecting strikes for a strangle in my latest report, hope it helps. Trading options is very flexible trading so no rules can be set in stone. But usually, I start with delta 10 to 15 to set my strikes and to collect at least 10% of the stock value (e.g. if the stock trades for $40 then 10% from 100 shares or $400 would be $40 or 0.40 credit I would like to get). The rest is pretty much mechanical. Then I monitor the trade and roll it if I do not want an assignment or need to release buying power.

Thanks. I just read that. I was curious about the closing mechanics (50%, etc) since you’re reinvesting that credit towards stocks, if you only reinvest half of your credit. Yep, i assumed we’d dive deeper as the challenge went on, but having a little extra capital to utilize, i was hoping to do a little more before our challenge got there. Thanks for the post and response!

Yes, I let the trade run to expiration and let it expire. I roll it if I see it may not expire safe OTM, then I roll it, but if it is safe, I let it expire. I reinvest the entire credit I received.

I think it’s smart to step away from 0DTE trades, they work until they don’t…you’re ‘staring down a train to pick up pennies’ as they say.

I agree. The problem is that when they stop working the losses are catastrophic compared to the gains. I tried to push it hard but failed. Time to trade what I know and what works for me.

Thanks for stopping by.

when you said in the monthly spx

1) DTE shall be 50 or more.

2) The IC width shall be 25.

3) The collected premium shall be $3 or more, the more the better

what do you mean by width shall be 25? the difference between the sell strikes (cal and put) to be 25? if you choose one side 10 delta, the other should be 25 strikes away? so if the sell call is 3555 and sell put should be 25 point away (3555-25 = 3530) but this will be ITM put and not OTM… just trying to understand how to construct it at 10 delta and get 3$ premium. any help is appreciated.

25 is the width between short and long leg of the option, that is 25 dollars, or 2500, So, if you sell 3000 put and buy long put, it is 25 below the short one thus 2975. Then the entire spread will be 3000 / 2975. Then you do the same on the call side. Let’s say you want to sell 3400 short call then you open 25 points call above the short one, thus 3425. The entire spread then will be 3400 / 3425 call spread. Both shorts (put and call) shall be at delta 10).

Martin,

I think I understand most of the statement above and makes perfect sense, except this part “Both shorts (put and call) shall be at delta 10).”

So on the example above the IC will look like this:

Buy 3425 Call

Sell 3400 Call

Sell 3000 Put

Buy 2975 Put

#1 Question: How did you derive the 10 delta? (can’t quite wrap my head around that part)

#2 Question: I see the width between selling 3400 Call vs selling 3000 put is $400 dollars…. Did you come up up with this number based on the support/resistance for the 1-2 months ?

Currently using Robinhood for the options at the moment.

Thanks again Martin for this take!

The option chain should show you current deltas. So you just go and find deltas 10 for each short option. See picture below for 57 DTE trade. So, if you find delta 10 you get your short legs, Then buy 25 points wide long legs. In this example, you will get a 750 points wide Iron Condor body with 25 points wide wings and collect 4.40 (or $440) credit.

Amazing! Thank you so much for explaining that Martin. Now it makes sense.

Also how do you usually best define the Short Call & Put Positions….let’s say for Weeklies ending in Friday and for Monthlies?

I was thinking support/resistance based on last 30-40 days.. thoughts?

I do this solely on delta but depending on the market outlook I may skew the trades to the market direction or omit one side completely. For example, in a strong bull market, I may choose higher delta on puts and skew calls higher or omit calls whatsoever.

Hi Martin,

I’ve got some doubts concerning your new strategy. Rolling untested side when the tested side reaches delta 30 is a no-go in practice. The untested side is so deep out-of-the money that you can’t trade it. This is particularly challenging for your 3-day strategy.

Could you please clarify it a bit?

Keep up great work !

Paul

On the contrary. When you roll untested down (calls) or up (puts) you collect more credit and offset the potential loss. At some point you end up having an Iron Fly strategy when your puts and calls (short) are at the same strike. I also use the credit to roll the tested side, these days. Works well. With SPX I do not have any problem rolling untested side closer to the tested one.

Thank you for all the work and guidelines you post here for free.

I had a look at the champions list and found it still needs a lot of screening as many stocks just don’t have enough option activity to be worth considering for put selling.

The champions list is mostly for purchasing the dividend stocks, so yes you need to screen them for being optionable. It is however difficult to find good optionable stocks. Those worth selling options on are in my Watch List.

Really cool website this.. have been reading a lot. I notice in your strategy rules above that there is only one that mentions any technical analysis. You mention looking for getting in around supports etc. What tools would you use for that? Just drawing lines or do you use any indicators at all?

Hi, I use Fibonacci levels and then draw supports and resistances based on the market behavior.

Thanks Martin, keep up the great info!

This is fantastic. Thank you!!

Thank you. Found your blog and it has been immensely informative.

Thank you. Hope it helps others to avoid my mistakes…

What are your thoughts on selling puts on a 3x fund such as TNA?

I guess it would by like trading any index. I would have to watch it for some time to see how its options react to the market moves. The only thing I do not like is that it is not marginable so trading June contract 60 strike you make 53 premiums and you will need 5,346 margin to trade it. Too much money for not much music.

Hello,

I’ve just found your website and read several posts. You’ve done a wonderful job of sharing and imparting your knowledge in a clear and concise read. Kudos for your commitment to assisting others in their efforts to trade options profitably.

One question I had though in your SPX trading strategy relates to the 40 dollar wide strikes you use. Your discussion of the logic in using the wider strikes seems to neglect one important metric in designing trades and that is margin impact.

If I choose to trade a Nov1 15 iron condor in SPX with short strikes of 1700/2200, using your 40 dollar wide strikes I get a trade that looks like this – 1660/1700/2220/2260. Using TOS, I right click on the trade, hit “confirm and send” and a dialogue box pops up which shows me I will get a $202.01 credit after commissions with a resulting buying power effect of ($3,797.99) which equates to a 5.31% return on risk.

If I then use the same short strikes but make the strikes 5 dollars wide, I get a trade that looks like this – 1695/1700/2220/2225. Now I adjust the number of contracts so it comes as close to the buying power effect above of ($3,797.99) and I get 8 contracts. Again, opening the dialogue box which summarizes the trade, it shows a credit of $246.01 after commissions with a resulting buying power effect of ($3,753.99) which equates to a 6.55% return on risk.

Isn’t that getting me more bang for my buck? Please consider the above scenario and see if I’ve missed something.

Keep up the good work.

Steve

Hi Steve, thank you for you kind words.

To you question, it is a matter of priorities. Yes with 8 contracts you get about $44 more or 1% more, but your risk losing entire credit is a lot higher than mine. As I tried to describe in the post, 5 dollar spread has a higher likeliness of the price smashing thru both strikes than 40 dollars spread. It is the same with 50% credit capturing strategy. When I receive $180 credit, why liquidating it at $90 and not keeping the entire credit and letting the trade expire worthless? Well, the numbers are against you and you will be better off with a wider spread and closing it at 50% credit although it looks better otherwise at first look. And actually it is not. Trading 5 dollars spread is OK if you do not have that margin available (I do not have it, so I only trade 10 dollars spread and working towards 40 dollar spread goal). So the entire spread width meaning lays in probability of success and not the immediate gain. I personally would prefer lesser gain but lower risk and higher probability of success than 1% more gain and a chance that if the trade goes against me I have higher chance of losing the entire risked spread.