Savvy people save money. It is an important part of everyone’s life and it shows how educated financially a person is. There are several ways, methods, and purposes for saving cash.

I learned saving cash at early age. When I was about 12 years old I was keen on building models of historical man-o-war sailing ships and I wanted to have all books about those ships and how they were built. My parents weren’t rich, and since those books were quite expensive, the only way to get the books was to save money.

|

Even today I am proud of the achievements I made at my early years, that I was able to buy those books on my own and without a help from my parents.

There are several purposes for saving money. People save for retirement, for a college, for kids and their college, and for all sort of goals, such as new car, house, new TV, etc.

It is all great and honorable if you do that. These days a lot of people use debt to purchase those items instead of saving for it first. So if you save first and spend later, then you are a unique person. But over time I learned that saving for recurring bills can help you to release a burden of your everyday tight budget. Yes you can save for smaller goals than a new TV or car. This article will focus on saving for this particular purpose – your larger recurring bills rather than the traditional goals.

Identify your large bills

Do you have bills which can bring a hardship to your budget? I do have some. As a mechanical engineer I am a member of a professional association (ASHRAE – American Society of Heating, Refrigerating and Air Conditioning Engineers) and I pay $190 membership dues every year. I also pay $450 home owners insurance yearly, $300 home owners association due/tax (or whatever it is), $236 life insurance semi-annually, $80 car registration plates annually, and many other large annual bills.

I bet you can find some in your own budget. These bills can be quite bothering if they arrive in the wrong time (they always arrive at the same time, but it may not be your time).

Split the bills before you get hit with a large one

Did you ever experienced a situation like mine which I experienced just recently when I have received a bill for homeowners association to pay $300 dollars and a few days later my insurance broker called me that they haven’t received a life insurance semi-annual payment and what happened? I was suddenly hit by two bills at the same time and I was supposed to come up with a payment totaling $536.

This amount looks small in an annual perspective, but it can be a significant deal at the current month, especially if you had a few other unexpected expenses (such as a car repair, which my wife paid for). Fortunately, I was ready for this situation, but it made me thinking what would happen if I wasn’t. I would have to use debt to pay for it.

Many years ago I decided to save for those bills and split them in smaller increments, which is easier to handle every month.

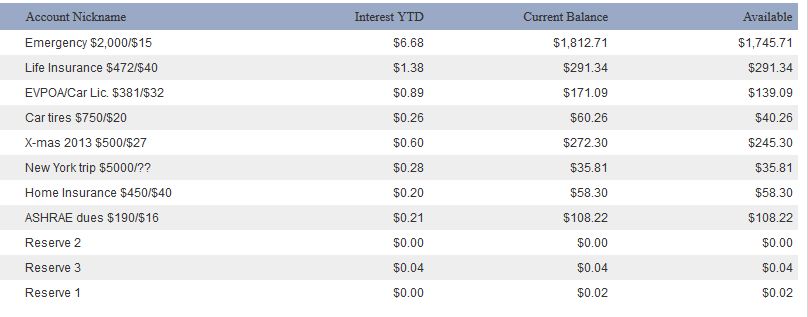

I opened several savings accounts and each has its own purpose. I even nick-named those accounts according to their purpose. For that I have an account named “Life Insurance $460/$40” “EVPOA/Car Lic. $381/$32” etc. The first number indicates what amount I need to save and the second number indicates how much money monthly I am saving for that purpose.

The math is easy. You take the annual amount and divide it by 12 months. That gets you how much money you have to save. For example, for the life insurance I have to save 460 dollars annually. That number divided by 12 gives you $38 a month. I save $40 and let the $2 accumulate over time into more cash available.

It is a lot easier to pay 40 dollars monthly than $230 semi-annually. This gives me a peace of mind and I can completely forget about this bill.

Pay yourself first

You may have heard this old adage “Pay yourself first”. That means that you take the cash away for savings from your account before you start spending it. In my opinion this is the most important part in saving money. I do this all the time. I set up an automatic deduction from my checking and the little cash is transferred into my savings accounts automatically. Every month. I no longer have to worry when my broker calls me that a payment hasn’t been made. I just gave him my credit card number, and later at home I transferred money from the savings account back to my checking and paid the credit card off.

Pay slightly more if you can

It is a good practice to save a bit more that you would be required. If your monthly amount should be $38 then you can pay $40 or even $45 a month instead. The reason behind this is that over time you accumulate more money, ideally one payment ahead. That will create your emergency savings. You will have one year payment in your account and only using cash you theoretically saved one year ago. Even greater peace of mind. Then you can reduce your monthly payments to the exact number and let the interest do its job (although in today’s interest rate environment the job is miniscule). You can redirect the surplus to a different account.

The bill arrived

It’s very easy process here when the bill arrives into your mail box or email. You can use your credit card to collect points for example or use a benefit of free 20 days grace period (squeeze that 0.000000001% interest the savings account gives you for another 20 days) and before the credit card company asks you to pay back, you transfer your saved cash back to your checking account and pay your credit card bill in full. Done. And you know your savings account is slowly accumulating for the next year.

Never use the money for a different purpose

Once you start saving cash for those bills, if you want to enjoy a peace of mind this method can provide, never, ever use that money for a different purpose. Never! You are saving for that particular bill and nothing else. That’s why I also am advocating to have separate accounts dedicated for that purpose rather than only one account with all the money pooled together. You would then need accounting and keep track of any contributions and expenditure. It may be tricky and it may get you into thinking that you have money saved, while you may actually be withdrawing money from a different “digital envelope” (purpose).

Conclusion

Saving for a specific purpose such as recurring large bills, typically paid annually, can help an investor offsetting a potential financial hardship and fear when such bill arrives that you not always have money aside to pay it. Having a specific savings account dedicated to the defined purpose may help you with budgeting without keeping the books, without messing up your emergency savings account, tapping into a pool of cash in your emergency account, or even worse taking a new debt. With this method you know exactly what you need, what you already have and what you spent. Saving small money monthly before you start spending other cash from your paycheck is a lot more affordable than one large bill once a year. When you have money saved and you know it and see it in your monthly statement, it gives you a great peace of mind. You no longer worry about that and any of the future bills anymore.

{kind=link}

Awesome thank you very much

Who says saving money is hard? By following your tips, the path becomes easier. The steps you have pointed out is going to be helpful for a lot of people.

David, thanks for your kind words. It works very well for me. I am not messing accounts together and all is clear and easy to follow for me.

When I started keeping track of all our income and expenses, it became much easier to save. We have a similar saving strategy as well and it’s working out well so far.

These are great tips. I especially like the idea of opening different accounts for those large annual bills and saving monthly for them. I haven’t actually done this myself (but should).

Straightforward advice Martin! What you do after you save money is just as important as the process you use to get there! Investing a large portion of your savings is key for building wealth.

And just to add to it, my ultimate goal on this is to save a year or two of the bill payment ahead. Then I know I have enough cash to overcome income disasters.

I agree. With this method I just continue saving and building cash reserves for the bills. But I use the same or similar strategy when saving for investing.

[…] Hello Suckers: The art of saving money […]

I’ve used this strategy a lot in my budgeting but I hadn’t considered adding extra to get one month ahead on annual bills. Thanks for that great idea – going to change that in my budget right now…

I am happy that you could get an idea out of the post. I like this strategy and have more cash saved to be able to cover one bill ahead in case something goes wrong. thanks for stopping by.

I use a similar strategy. I keep my emergency fund in a totally different account than savings that I’d tap for things like a vacation or other purchase I’d set a goal for.

I like keeping those savings in several accounts. In that case the savings is all clear and visible. You know exactly what you have.

Very good plan of attack for the unexpected. I learned this, like so many, the hard way. Being self-employed, the potential for annual insurance renewals and other payroll expenses, not to mention income taxes, can destroy an otherwise profitable business.

This post could easily have substitued “Budgeting” for “Saving” and it would be equally helpful and applicable. Thanks!

Curtis, thanks for stopping by. I learned this the hard way too. Considering that you are self employed, I wouldn’t imagine managing my money different way. Thanks for stopping by.

This is great advice. I utilitize a very similar strategy to you. My wife and I have an account for each major bill or purchase we have on the radar. It’s great to know that when the bill comes up all we have to do is pay it out of the account that is designated for that bill. It’s already been taken out of our regular account, so I feel like the money has already been spent. It amazing what a simple change in managing your money can do for your peace of mind.

Jake, I agree. This provides me with excellent peace of mind knowing that I have money saved for every bill. Thanks for stopping by.

Very solid advice for saving. You definitely have to pay yourself and, as you say, squeeze as much out as you can for that. We also have separate accounts for long term goals and short term bills so we don’t touch any of the long term money.

We recently were able to change our insurance payment to monthly with no added cost so that we could avoid the situation you mention of a quarterly or semi-annual bill coming in that could mess with the monthly budgeting.

Greg, thanks for stopping by. Some insurance provide you with discounts when you pay annually than monthly. I do not know how that works and why, but I could have cheaper premium, so I decided to stay with semi-annual payments. With this strategy of saving I do not care at all how it is paid though.