April 2016 was a positive month to me. Both account – trading account and my ROTH IRA dividend account grew well and nice.

Surprisingly nice! There are a few patterns I start seeing which makes me happy.

I hope, that it will stay like this in the coming month although last day of trading in Wall Street put a little blow to my trading account.

Nevertheless, my options trading account ended up 32.60% in April and I made collected $938.00 dollars in premiums.

My dividend investing was slower than that (but I do not expect any fast and huge profits) yet it ended up by amazing 7.96% and I collected nice $84.49 dollars in dividends.

I also do options trading in my ROTH account and I collected additional $90 dollars premium.

Let’s take a look at the details!

You may be interested in:

Not in our portfolio By Bryan with Income Surfer

Recent Transfer: Raytheon Company By FerdiS with DivGro

Three Oversold Dividend Stocks By Dennis with Dennis McCain Investing

Find Out How You Can RETIRE SOONER with My New eBook By MMD with My Money Desing

Recent Stock Purchase April 2016 By Keith with DivHut

Dividends Earned – April 2016 By Investment Hunting with Investment Hunting

· April 2016 trading results

April trading ended great with nice profits. I traded options against dividend stocks and I traded aggressively selling ATM puts collecting premiums. This aggressive trading put a few stocks in a heat.

I accepted assignment of Ensco (ESV). I didn’t have to and I could roll the option, but I wanted to accept it and keep the stock and trade against it. I continue selling puts and covered calls. Hopefuly, I will also collect dividends.

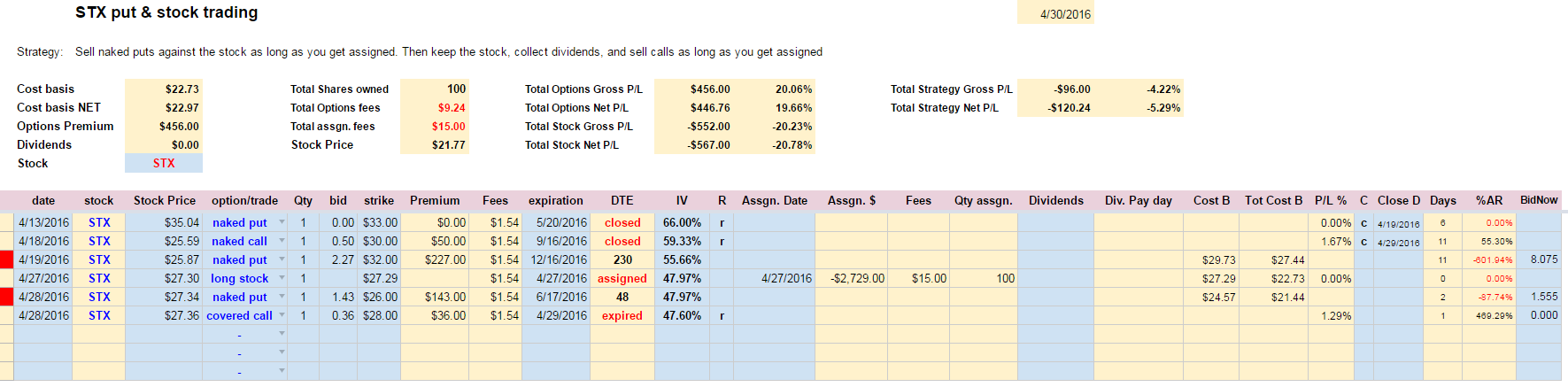

The biggest heat I got was from STX. What at first looked like a good trade ended bad. First, the company lowered its outlook and the stock tanked making my puts in the money. Then it started recovering and you could see the short selling squeeze. The stock rallied and I decided to cover my naked calls by buying shares of the stock.

I also sold a few more puts. Then earnings blew the stock out of the water and it tanked 20%. Another over-reaction from the market. I think we need to get used to it that investors and traders will react like this. It will be a reaction from one extreme to another.

But the most important thing is, that if something like this happen a trader must know what to do and not to panic. Always have a plan. Always have a plan for every situation in the market. Always know what steps you want to take to mitigate the loss or eliminate it.

To my STX trade such plan is to stay the course, roll the puts lower and continue selling more calls and puts. I opened my first trade at 33 strike. I could lower it down to 32 strike and I plan lowering it more down to 31, 30, and so on. And if I get assigned early, I’ll take the stock, keep it, collect dividends, and continue selling covered calls.

Here is my trading result for the month:

| April 2016 options trading income: |

$938.00 (36.93%) |

| 2016 portfolio Net-Liq: |

$3,039.46 (32.60%) |

| 2016 portfolio Cash Value: |

$429.69 (-87.47%) |

| 2016 overall trading account result: |

19.68% |

My cash value dropped because of purchasing equity. I was assigned to ESV and purchased STX this month. That’s what the cash was used for.

Here are the results of my options trading:

(Click to enlarge)

Here are the results of my options strategy:

(Click to enlarge)

The table above shows a good strike of winning trades in the first quarter. I hope my next quarter will be as good as the last one.

My average trade holding time is currently 19 days, average P/L 3.11% and 111.27% annualized return.

Not bad results for only two months of trading after I returned back to this strategy.

I knew trading SPX spreads wasn’t for me and I should have stayed with my original strategy (this strategy) in the first place. I could have been a lot further ahead, closer to my retirement. But we are human, we make mistakes and we are here to correct them, start over, and move on.

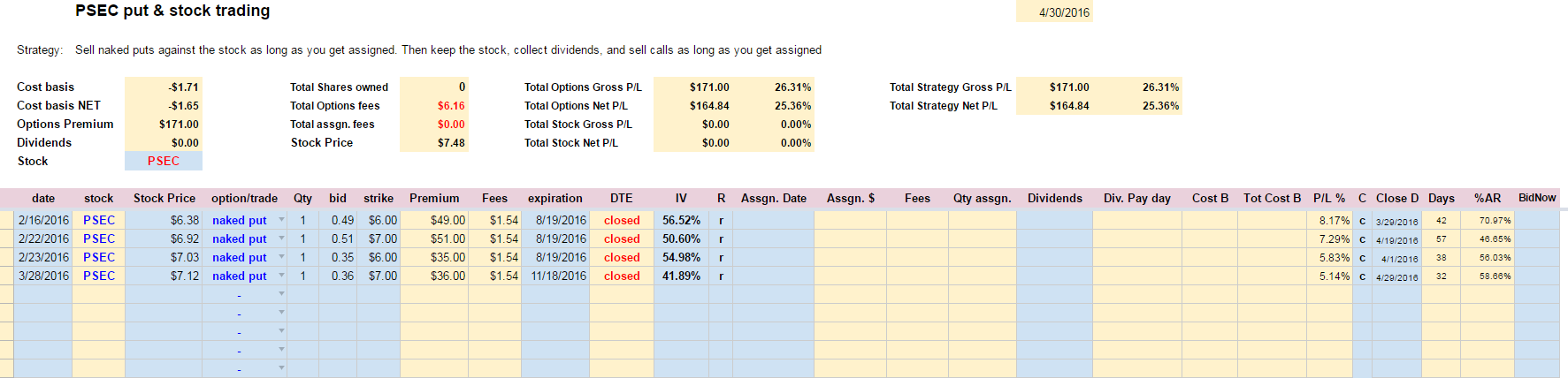

Here are results of the individual trades:

PSEC

(Click to enlarge)

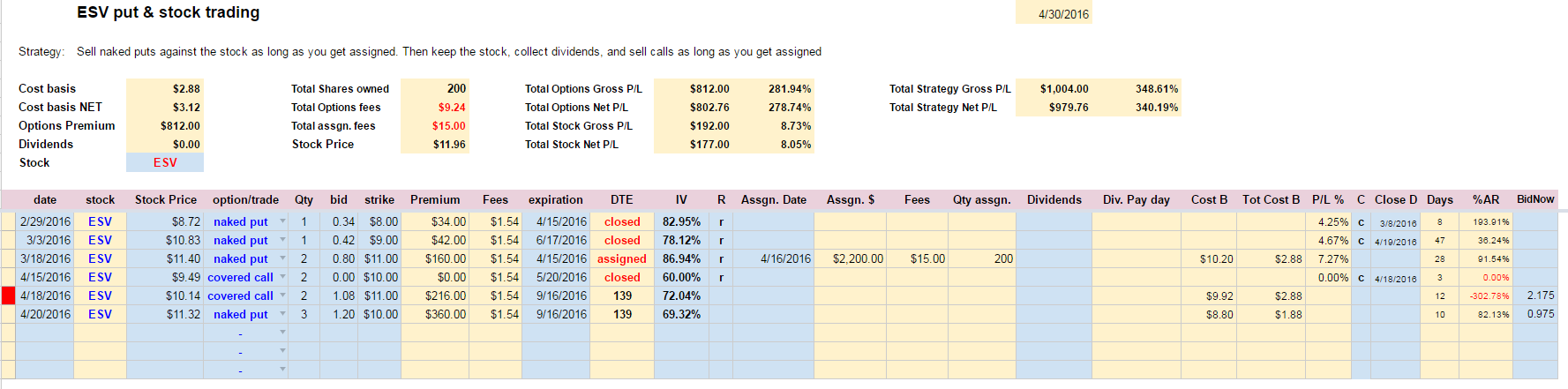

ESV

(Click to enlarge)

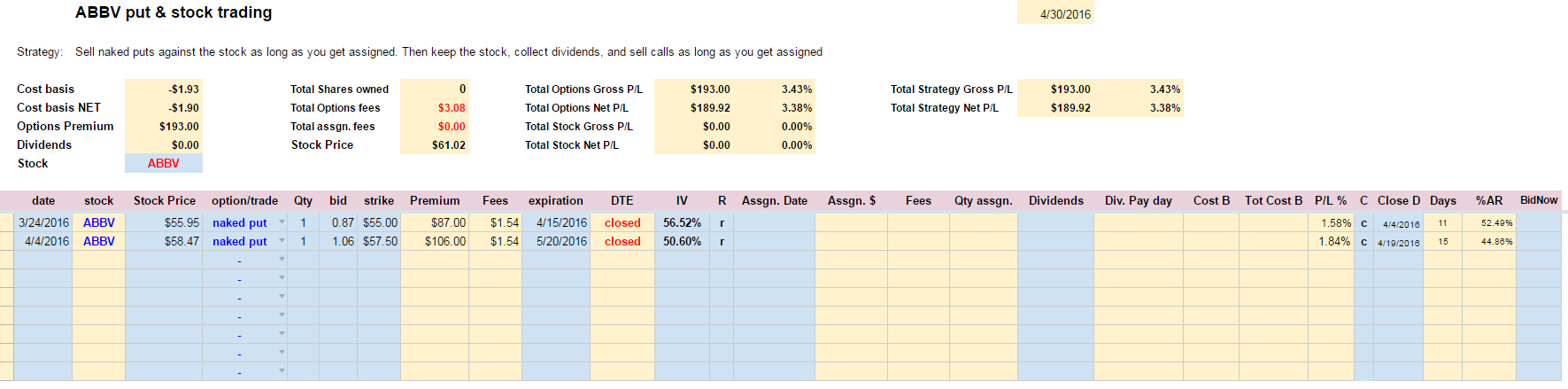

ABBV

(Click to enlarge)

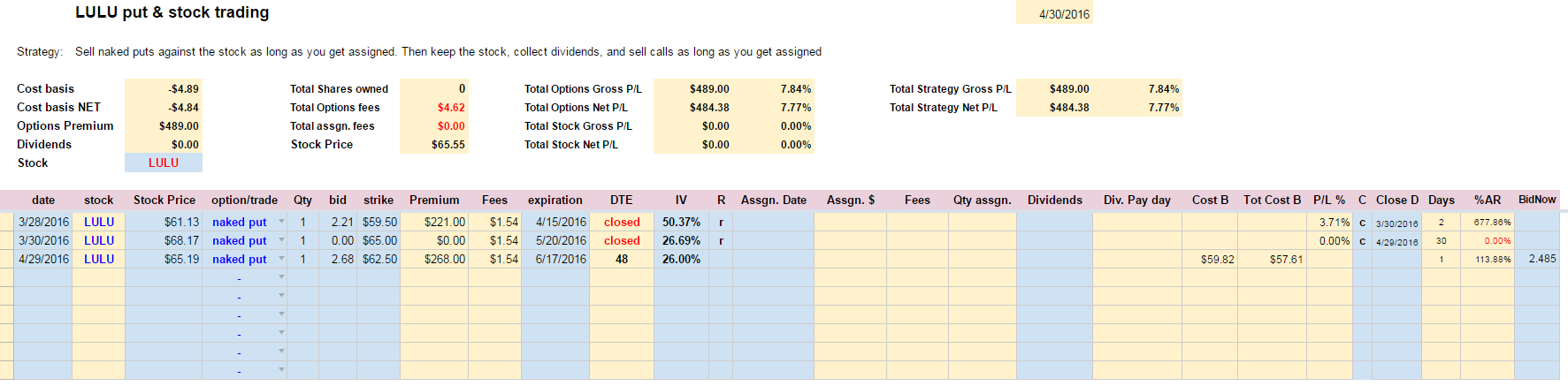

LULU

(Click to enlarge)

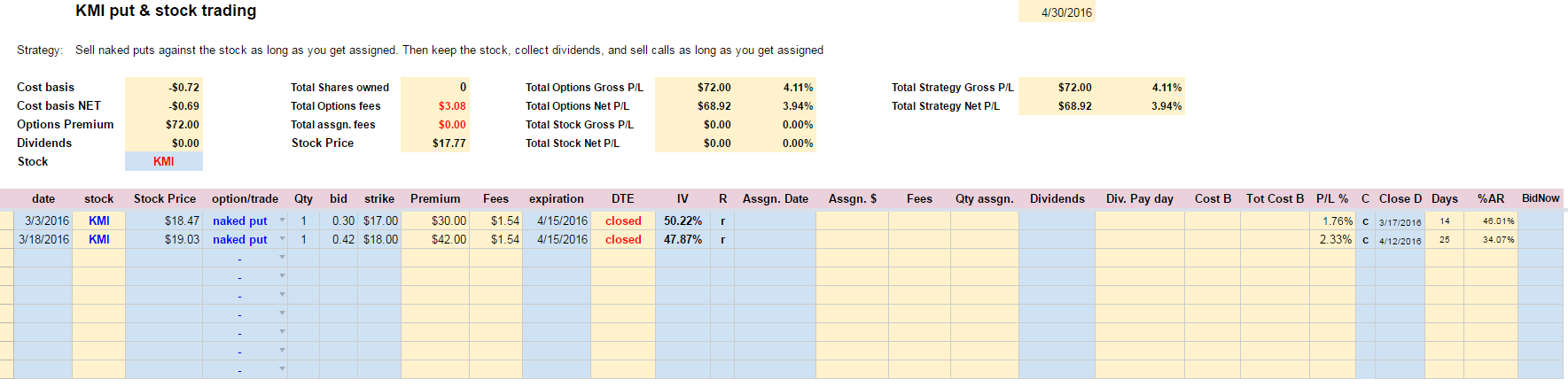

KMI

(Click to enlarge)

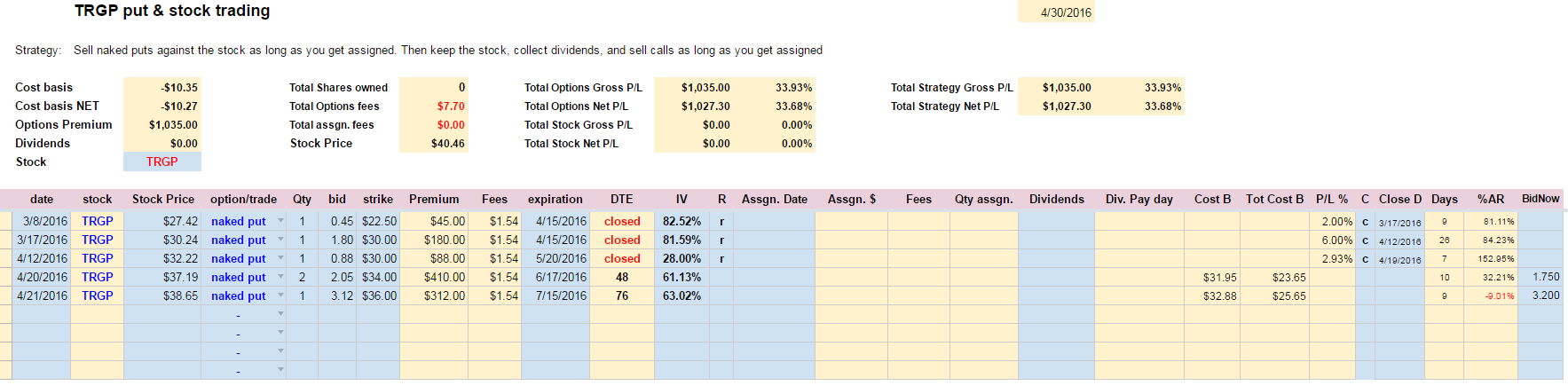

TRGP

(Click to enlarge)

COP

(Click to enlarge)

ETE

(Click to enlarge)

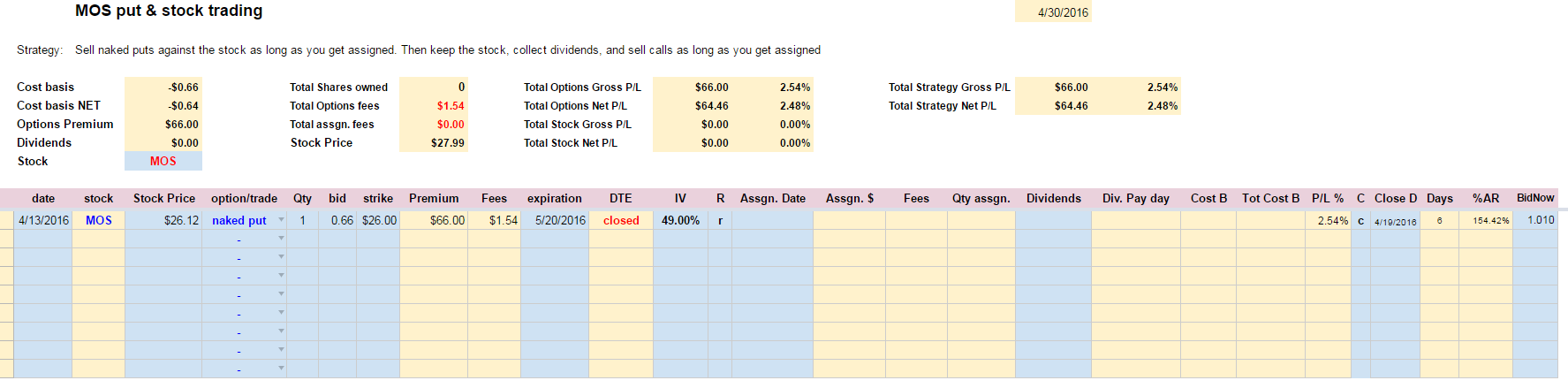

MOS

(Click to enlarge)

PSX

(Click to enlarge)

STX

(Click to enlarge)

If you like these trades and want to be informed when I place them and trade them in real time, you can join our closed Facebook Group. The group is a closed group and there are other traders posting their trade ideas too. We learn from each other, eventually ask questions, get answers, but most importantly you can see what we trade and how. You can follow those trades.

Here is the entire account value from the beginning of tracking it up to today:

You may be interested in:

Building Failure Into Your Process By Ben with A Wealth of Common Sense

Portfolio Update: Gold Mining Stocks (April 28, 2016) By FIF with FI Fighter

The Normality is Called Volatility By Mike with The Dividend Guy

Options Expiration – April 2016 By Alex with My Trader’s Journal

April 2016 Dividend Income By Adam with I Want to Retire Soon

· April 2016 dividend investing results

After dividend cuts my portfolio stabilized and is steadily growing again. I liked a lot seeing my DRIP purchasing, seeing that I am purchasing more and more shares and those shares are producing more and more dividends every month.

Just recently I was looking at some of my holdings and I saw them bringing in more dividends. It is most visible in monthly paying stocks that every month I get slightly more dividends. And I can see this process speeding up significantly.

What do you think?

To me, this is very motivating to continue building my dividend portfolio although I am more into options rather than being passive, working hard, putting money into my account and waiting.

I want options trading doing this job. I want to trade options, take all proceeds and invest them into dividend stocks. Then I do not have to work hard skip vacations because I am saving money.

I am lazy, and I want my money not to be lazy.

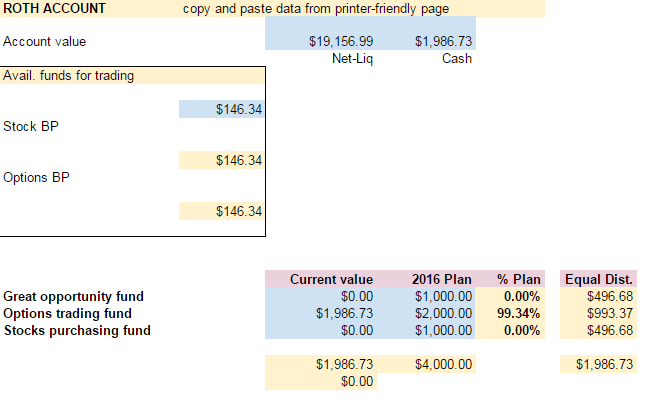

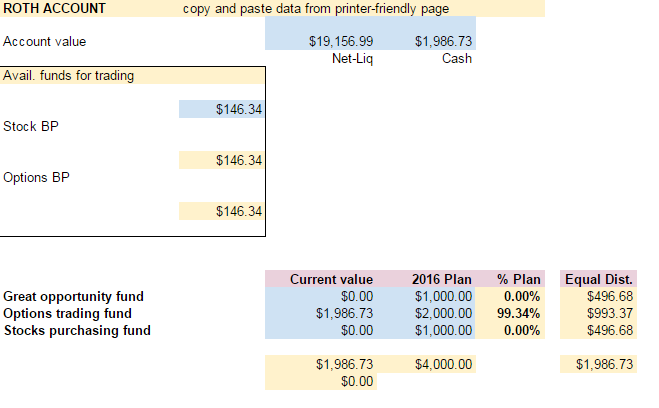

For this reason I created three sub-accounts in my ROTH account.

Those accounts are mental accounts. Physically they do not exist.

I keep it only in my spreadsheet and keep track of it.

So I created a “fund” of a “great opportunity”, a fund for “options trading” and a “stock purchase” fund. As of now, I plan to keep $2,000 for trading options (and slowly increasing this “account”, $1,000 dollars for great opportunity (if any good stock suffers from an irrational selloff, I want to have some cash ready for this event), and stock purchasing “account” will be an account which I will use to buy stocks out right. Once filled with cash, I use it right away to buy a stock of my interest and then continue saving new money.

And guess which account would make money for those two other accounts?

You got it, it is my options trading account. Here is a picture of my ROTH IRA account spreadsheet I keep track of these sub-accounts. Now I am in a re-filling or building those sub-accounts:

(Click to enlarge)

As you can see, my “options trading account” is almost funded. Once funded, I will continue trading options using this money, but all proceeds will be allocated into “great opportunity” fund. After that fund is funded, I will be allocating all proceeds and savings to “stock purchasing fund”.

I will also be increasing goals in those funds as my options trading will be growing.

(Click to enlarge)

My annual dividend income this month is up from $887.98 to $897.17.

Dividend stocks added or removed from portfolio:

| April 2016 dividend stock buys: |

none |

| April 2016 dividend stock sells: |

none |

To purchase stocks I use trailing stock order strategy OTO trade order (one triggers other) and I described this strategy in my post about purchasing stocks in falling markets.

I also invest into dividend paying stocks using Motif investing which allows me to buy all 30 stocks I want in one purchase using fractional investing, similar to a mutual fund.

You can actually build your own mutual fund with Motif investing.

Here is my Motif Investing account you can review:

I continue reinvesting my dividends using DRIP program. I love how my holdings grow when reinvesting the dividends and when the stock prices are going lower. As I believe we are heading into a recession I will be able buying more shares for a lot cheaper.

Dividend stocks DRIP:

| April 2016 DRIP: |

Reynolds American Inc. (RAI)

PPL Corporation (PPL)

American Capital Agency Corp. (AGNC)

Realty Income Corporation (O)

Prospect Capital Corporation (PSEC)

|

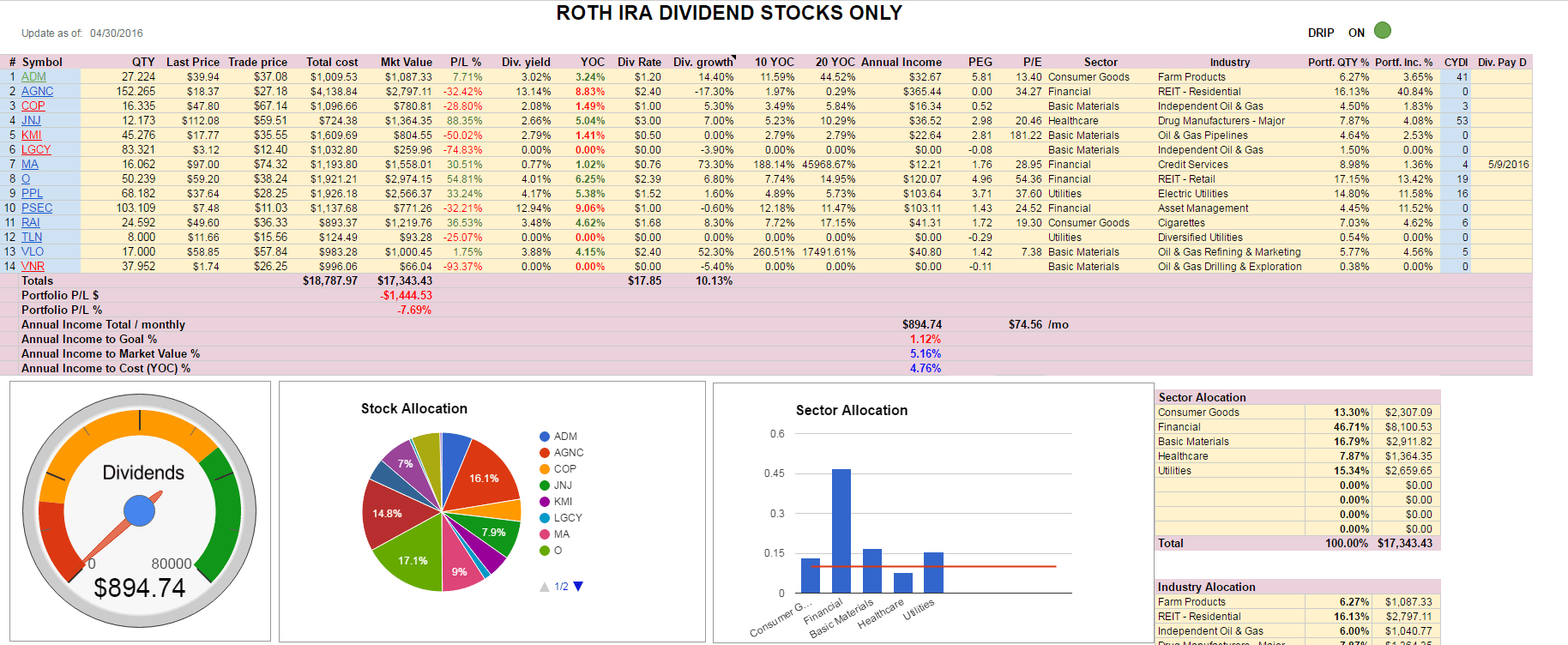

Here are my ROTH IRA trading/investing results:

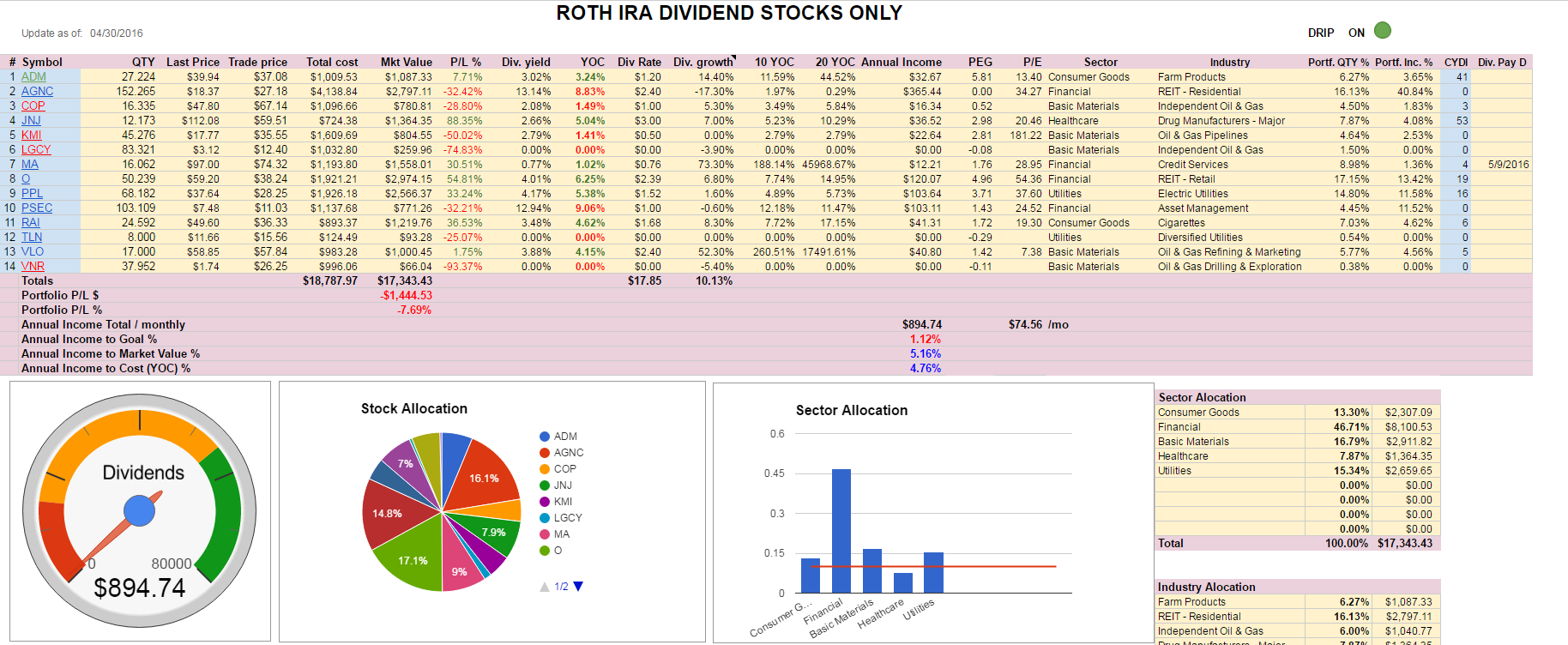

| April 2016 dividend income: |

$84.49 |

| April 2016 options income: |

$90.00 |

| 2016 portfolio value: |

$19,156.99 (7.96%) |

| 2016 overall dividend account result: |

26.53% |

The account grew by 7.96% from last month, overall I am up 26.53%. Dividend income was also up from last month. All dividends were reinvested back to the companies which generated them.

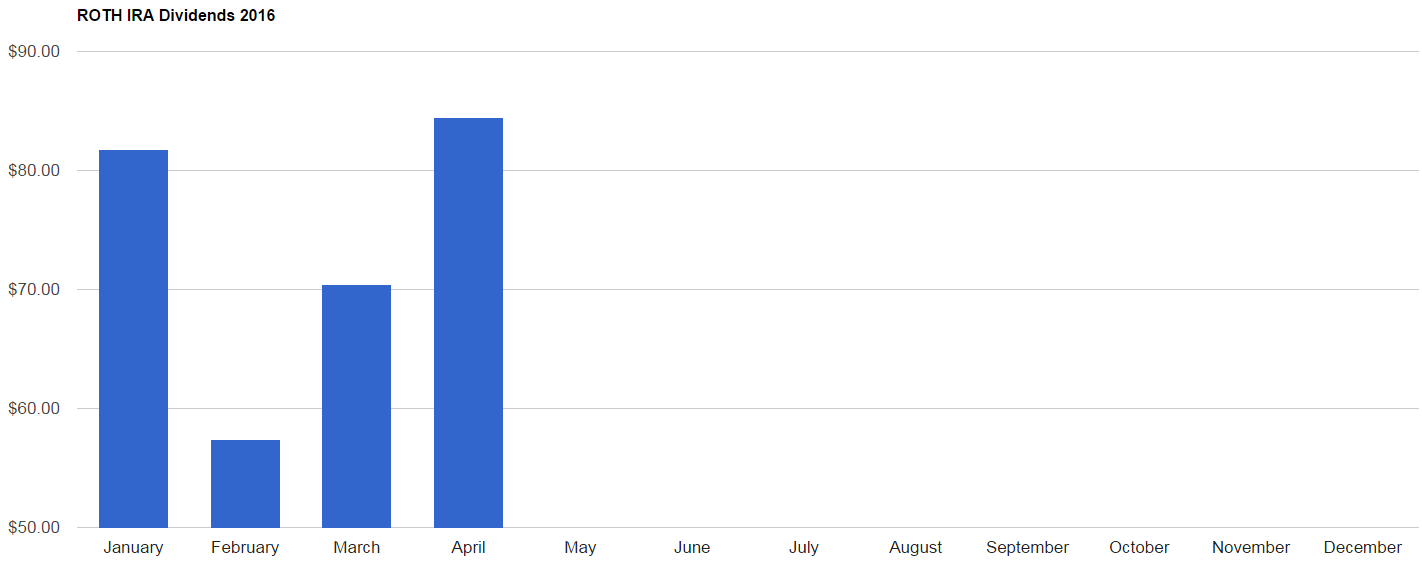

Here is my dividend income:

Annual dividends since the beginning:

Here is the entire account value from the beginning of tracking it up to today:

You may be interested in:

Revenue in April 2016 By Chris with Easy Dividends

Monthly Review – April 2016 By David with David’s Financial Freedom Journey

Monthly Review – April 2016 By R2R with Roadmap2Retire

Trade Ideas & Chart Analysis For The Week Ahead, May 2nd to 6th 2016 By Nial with Learn to Trade The Market

Dealing with loosing option trades By ambertreeleaves with ambertreeleaves

Below is my dividend income review for the entire year:

My ROTH IRA dividend income breakdown per month and per company.

· All accounts

Besides trading and dividend accounts I also have 401k account, emergency savings account, etc., which I do not report in detail. You can review those accounts in my “All Accounts Value” table at the bottom of My Trades & Income page.

My accounts increased from previous month and are making 16.58% (up 5.69% from previous month) for the year.

Remember, if you like trading options and want to have trade ideas for free, join my Facebook closed group and follow my put selling trade ideas in real time, comment, ask questions, and interact with other members. Other members of the group can also post their trades so you can learn from them too.

What do you think?

How about your investing or trading results?

Do you have any question? Need help to start trading or investing? Shoot me an email or let me know below in comments how I can help you.

We all want to hear your opinion on the article above:

7 Comments |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Recent Comments