I once held in my portfolio a stock which paid nice dividend and had a promising outcome as monthly dividend payer. Right before it collapsed. I was fortunate enough to get rid of the stock before it actually happened. I am talking about mREIT stock Armour Residential (ARR). This stock can be a great example of what to avoid and what not to do.

Although I do not own this stock anymore and here I wrote my reasons why I sold it I still like to watch this stock. I still have it in my watch list, charts, and I still visit a message board on Yahoo to read what others have to say about this stock.

I know that reading Yahoo message boards about any stock is a waste of time and there may be a lot of unreliable information, I still could get some great ideas out of there to think of.

One idea was that people do not understand mREITs and they shouldn’t invest in stocks such as ARR.

True. I do not understand mREITs. All I know that they make money by an interest rate spread between short term and long term mortgages they trade. I am not sure how exactly they do it, but they seem to be borrowing money on short term contracts and finance long term mortgages. If the 15 year mortgage rate is currently around 2.75% and the long term is at 4% (the numbers I am using here are not accurate and I used them just to illustrate the point), they make whatever the difference between these two numbers is.

How the information about mREITs business model can help you to determine whether it makes sense to invest in ARR?

If you have time to spare and browse thru the message board about this stock, you get the impression that this stock has a lot of value and you know absolutely nothing about investing into mREITs. The stock trades at $4.85 a share and its estimated book value is at $5.50 a share. So many will argue with you that if you have bought below $5 a share you were buying at a great discount and you cannot lose. On top of that you would receive a hefty dividend every month. What can go wrong, right?

If you have time to spare and browse thru the message board about this stock, you get the impression that this stock has a lot of value and you know absolutely nothing about investing into mREITs. The stock trades at $4.85 a share and its estimated book value is at $5.50 a share. So many will argue with you that if you have bought below $5 a share you were buying at a great discount and you cannot lose. On top of that you would receive a hefty dividend every month. What can go wrong, right?

I really do know nothing about mREITs, actually this particular mREIT stock. I am just a simple dumb dividend investor, who at some point decided to stop trading stocks, because he was losing money doing that and started investing into dividend paying stocks using buy & hold strategy (and in my earlier posts on this block you will be able to find that I was against this strategy during 2008-2009). So ignoring the fact, that I do not trade and I do not buy preferred stocks of ARR, what’s left? The only what’s left is to buy ARR, hold, and collect hefty dividends.

Those who now say ARR has value in this stock, because it trades at discount to its BV I would like to know, what is the difference between today’s book value and price and a book value and price a few months ago?

A few months ago, the book value was at circa $7.8 a share (I do not have the very exact number) and the stock traded around this price. Then the company issued SPO (secondary public offering) and it came out that the new BV was $6.8 a share. The stock tanked to $6.5 a share. then a dividend cut from monthly rate of 0.08 to 0.07 and the stock tanked further down to $6.0 a share.

Per the logic above this was a great value! The BV was at 6.8, the stock traded at 6! and the yield was 14% even after the cut!

Later the whole sector got hit by an irrational fear of FED ending the stimulus (which actually may be positive to mREITs rather than negative) and the stock tanked even more.

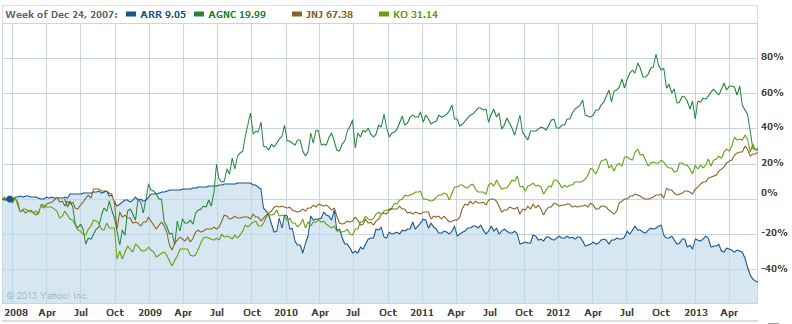

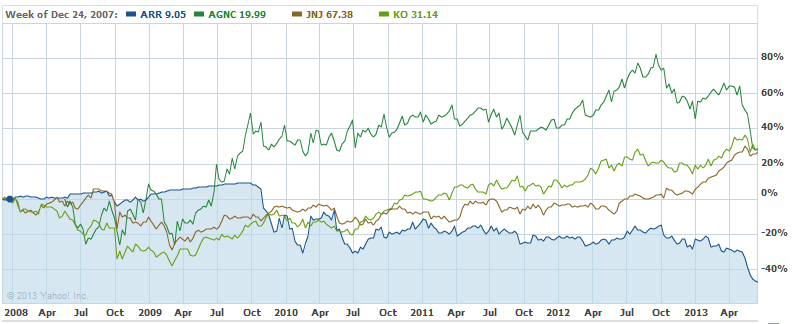

Let’s take a look at price action history:

This is the whole stock history. I try to keep my decision making simple and one of the metrics I look at is how the stock performed in the past. Although the past performance is not a guarantee of the future as every disclosure is telling you, I believe there is a clue in the past performance from the long term perspective. You can see from the chart whether the stock is steadily rising, going sideways, bumpy, or declining and in what time frame this is happening.

A human mind has a tendency to prorate such behavior into the future. You may be wrong on that, but from a 20 – 30 year time perspective you can easily see, what the stock was doing and what most likely will be doing in the next period. Although it is not a 100% guarantee that it will really happen, it is a solid clue how the stock may perform.

When taking look at ARR chart and compare it with any other dividend paying stock such as JNJ, KO, or even AGNC (the closest competitor of ARR), you will see a totally different picture:

(Click to enlarge)

From the price action I can see that no matter when I would ever buy into ARR, I would be sitting in a losing position. Unfortunately, monthly dividends wouldn’t be able to make up for the capital loss.

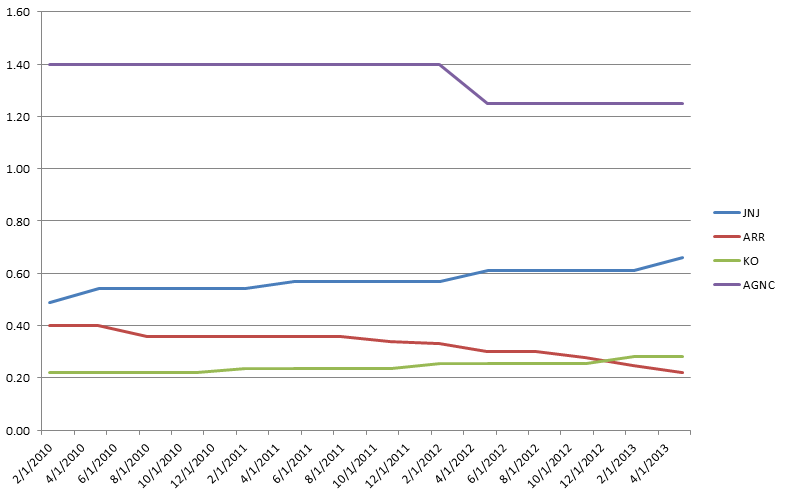

Let’s take a look at another chart:

(Click to enlarge)

The chart shows dividend growth for each stock for the same period (ARR adjusted to quarterly dividend).

Summary of reasons why not to invest in ARR

- The company provided several SPOs over the time of its existence diluting shareholders.

- The company was cutting its dividend since the beginning and never increased it.

- The company’s book value was declining since the beginning.

- The dividend cuts along with declining BV ended up in a constant price loss (currently the stock has lost 47%).

- The dividends were never able to keep up with the capital loss. the best outcome you could get is to get break even.

I really do not understand mREITs, because I do not see, how a dividend investor could ever make money investing in this stock. Asking some of those in the Yahoo message board makes no sence, because they will immediately tell you, that you have no clue how to invest in ARR. With AGNC, which I own in my ROTH account and although they cut their dividends I have at least capital gains, so it make sense for me to stay invested. But ARR?

Well, do you know and understand how these investors invest in stocks such as ARR?

We all want to hear your opinion on the article above:

1 Comment |

Server Yahoo posted several articles this morning in reaction to Mr. Market’s behavior today asking a basic question: “Is the market overreacting?”

Server Yahoo posted several articles this morning in reaction to Mr. Market’s behavior today asking a basic question: “Is the market overreacting?”

{kind=link}

{kind=link}

{kind=link}

Recent Comments