|

We all want to hear your opinion on the article above: No Comments |

When bitcoin inevitably crashes, inexperienced investors who believed the hype could lose everything.

Originally published by Vivek Wadhwa on LinkedIn: “Why Bitcoin Is the Largest Ponzi Scheme in Human History”

During the late ’90s, Silicon Valley venture capitalists and New York City investment bankers used phrases such as “monetizing eyeballs,” “stickiness,” and “B2C” to justify the ridiculous valuations of internet companies. They claimed conventional methods were inapplicable in valuing the dot-com companies — which had no revenue — because we were entering an entirely new economy.

Believing these people, and afraid to miss out on the gold rush, small-time investors, grandma and grandpa, and barbers and taxi drivers invested their life savings in companies such as Pets.com, Webvan, and eToys. The bubble burst, and they lost everything. Through a transfer of wealth in the billions of dollars from Main Street to Wall Street, VCs, unscrupulous CEOs, and bankers had effectively enriched themselves at the expense of hundreds of thousands of ordinary investors, leaving them to despair about their futures.

History is repeating itself now with bitcoin. This time, it isn’t just Main Street USA that is about to lose its shirt; it is also the developing world. Technology has made it possible for hypesters in Silicon Valley, China, and New York City to fleece anyone, anywhere, who has a bank account and an internet connection.

The story that bitcoin victims are being sold is that, because we cannot trust government-issued currencies, bitcoin is the future of money. One investor calls bitcoin “a gift from God to help humanity sort out the mess it has made with its money.” A PayPal director predicts that bitcoin’s price will reach $1 million in the next five to 10 years; asset managers say it is the new gold.

This is complete nonsense. Yes, the price of bitcoin may yet double or even quadruple — because its price is based on pure speculation, and these stories are feeding such speculation. But bitcoin’s market price is almost certain at some point to crash and burn, just as the dot-coms’ did, and for the same reason: because it is all hype. And there will be no one to turn to when it does, because no government or bank is backing bitcoin up; and the people who are hyping bitcoin will have cashed out and be long gone.

Bitcoin’s price is not a reflection of its growing usage as currency; it reflects merely demand for the mirage of its speculative value. Its price is rising only because people all over the world are hearing stories of how others doubled or tripled their money in a short period — and they don’t want to miss out. Unsophisticated investors are taking out loans to buy bitcoins. Those who have spent the currency feel remorseful when they see its price subsequently increase, so they hoard it.

Bitcoin was invented by an unknown person or group to be a digital currency. It allows money to be transferred directly between individuals using cryptography. The bank ledger is distributed to all users, and complex mathematical transactions ensure transaction integrity. Such a system makes it difficult for governments to know the identities of people exchanging money, so it has become a haven for money laundering, drug dealing, and corruption.

Beyond its usability for crime, bitcoin has major design flaws:

Continue reading the story here

|

We all want to hear your opinion on the article above: No Comments |

When you work hard, you set the law of cause and effect to work for you. If you work for a corporation, you will slowly start to improve your position within the company; and if run your own business, you will slowly start to generate more business. While working hard will set things in motion, working smart will speed them up. You will produce more and earn more for every hour you work when you become more focused, disciplined, and systematic.

Yet despite the merits of working well and productively, this is just the beginning of your wealth journey. Exchanging time for dollars has a serious constraint: your cash-flow will slow as fatigue set in. Additionally, there are only so many hours in a day that you can work. So, at some point, you must learn how to use your money to make money. You must learn to become an investor.

3 Basic Steps to Becoming an Investor

Step #1: Increase the difference between money coming in and the money going out.

Before you learn how to invest, you have to get better at managing your money. Basically, master the art of earning more than you spend.

There are two benefits to learning how to manage your money better: first, you will be able to set aside money, put it in a savings account, and then use this as seed money to begin investing; second, once you learn how to budget a small amount of money, it will be easier to handle large amounts of money–because the principles are the same.

Here are some ways that you can get better at money management:

1) Bundle your services to save money. AT&T (NYSE: T) provides a good example of how to build a better bundle. AT&T internet plans allow you to stream TV from up to five devices, obtain HD DVR, and get a Wi-Fi Gateway router for less than $100 a month.

2) Reduce your daily food costs. You can still eat well without paying as much for it. Simply take your lunch to work rather than eating at a deli and make your own coffee rather than stopping at Starbucks (Nasdaq: SBUX).

3) Track all your expenses for a month, and then distinguish between fixed and variable costs. Fixed costs are costs that you must pay for a service that you need. For instance, your phone bill is a fixed cost. A variable cost is a cost that you can decide to pay or not pay. For instance, paying for an online membership for an educational or entertainment program is something you are free to discontinue without serious consequences. Once you have a better understanding of your costs, you can decide if there is a cheaper alternative to your fixed costs and if you really need to keep all your variable costs.

Step #2. Increase your knowledge about investments.

Although advertising by brokerages might give you the impression that all you need to do well is to find the right adviser, it's not that simple. If you only rely on the financial expertise of others, you will have no idea whether you are paying too much in fees or buying the best investments. However, even if you are fortunate enough to find a good broker, then you are completely dependent on them as your source of wealth. It’s much better to become an expert in your own right and to ask brokers to give you a second opinion and facilitate your transactions.

The reason why some investors become really wealthy is that they are in charge of their own investments. They know what they are doing because they have a deep understanding of investment vehicles and the markets.

Step #3. Increase your experience with investments.

Once you have acquired a sufficient amount of knowledge with investing, you need to gain experience. Theoretical assumptions rarely match reality. When you begin, start small. If, for example, you are investing in the stock market, start with paper trading; or, if you are investing in real estate, buy a small property before increasing the size of your purchases.

In closing, set goals. If you have clear, written goals, follow these 3 steps, and choose to learn from your mistakes, you will achieve your goals of financial independence and follow your dreams.

|

We all want to hear your opinion on the article above: 2 Comments |

December 2017 ended and the whole year with it. It is time once again to review our goals and determine what we accomplished and what we have left untouched.

Our 2017 year was a prosperous but challenging year. On personal note my family and I experienced a lot of changes and also difficulties but I believe, these are behind us. It was a difficult year.

I had to change my job and move for another one (I still hope, one day in a not so distant future, I will be able to trade full time). I thought it could happen in 2017 but once again Mr. Market taught me a lesson. How many lessons will I have to take before I finally get to the end of this race and finish my goal?

I think, I learned yet another trading lesson. I learned patience and discipline. Something, I was ignoring for years and Mr. Market made me pay for it.

What was it?

Many times I wrote and advocated to fellow investors to stay small and not over trade. Yet, I myself was breaking that rule. Many times I told investors: “Do not trade more than 50% of your account.” But many times I went way over that number in my own account.

Our business account is still way stretched and I am battling hard to bring it back in line with my rules. And when I am this badly stretched, it is hard to do so.

I set my goals for 2018 already and I think it will be a prosperous year. The US economy is growing and accelerating (many “valuation gurus” chose to ignore it and they started liquidating their portfolios in preparation for a bad year. I think they will miss a good year). But, it doesn’t matter whether the next year will be good or bad.

What matters is whether you are prepared.

You have to have a goal and plan. I have read a good saying by John Galbraith “Everybody is a buy and hold dividend investor until the next bear market.” What a wisdom and truth in this sentence. When the bear market “hits the fan” everybody panics and start selling. So I am prepared in two ways:

1) Buy and hold high quality dividend aristocrats which proved themselves during last crisis. Stocks like JNJ, O, MA, ADM, KO, MCD, and many others survived not only 2008 crisis but also 2003, 1987 and some even 1932 crisis and came out as winners. Arguments that you may lose 50% of your portfolio during selloff are silly. Yes, you will lose 50% (maybe) but for how long? Most crisis do not last longer than a year and a half. Even 2008 which was the longest one took 16 months only. And look where are we today. My preparedness is to stay invested, reinvest dividends, and eventually buy more shares. Let the other panicking and handing us their cheap shares.

2) As an options trader the preparedness is in being able to reverse all my put trades into call trades (short puts and calls) and eventually reduce amount of trading by opening fewer trades.

We are looking forward into 2018 year with optimism, goals, and improved strategy laid out.

So what the last month of the year looked like? I can conclude that it was gear and successful month again.

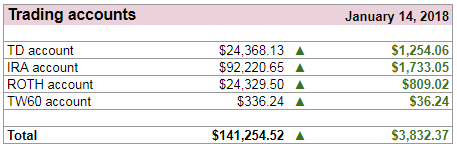

As of today, I manage four accounts (my own) and one client account. Here is a list of accounts I manage and review in my monthly reviews her on this blog:

TD – Ameritrade – business trading account, taxable

Traditional IRA – Tastyworks – personal retirement account, pre-tax deferred, former 401k account

ROTH IRA – Tastyworks – personal retirement account, after-tax deferred

TW60 – Tastyworks – personal trading account, after-tax deferred

Lending Club – P2P lending, taxable

December 2017 was a very good month and I made good income trading options. Let’s take a look at each account individually:

In the past few months I set a goal to bring this account back in line with my rules. I had to adjust some trades, take a few losses (not extremely large) which, fortunately, had no impact to the account net-liq, in order to accomplish this goal. At the end of December 2017 I can announce that I have accomplished this goal.

This account is now ready for trading and investing according to our trading strategy which you can find on our strategy page. In short, the strategy is to keep selling cash covered puts (or spreads) to generate income which can be reinvested into high quality dividend stocks. If you are a follower of our block since 2008 you may remember that this was our goal since then. Sad, it took 10 years to learn the process and get to this stage of trading and investing. This is a true university studies with a doctorate at the end! If you want to become a lawyer, you will probably spend 10 years in school too.

I think, I can claim, we are there and this account is finally growing again and generating income.

| December 2017 net-liq: | $23,520.48 ▲ | (up by $499.97 2.17%) |

| December 2017 dividends: | $74.92 ▼ | (down from previous $87.09) |

| December 2017 options: | -$132.00 ▼ | (down from previous $125.00) |

| XIRR: | 9.33% ▲ | |

| 2017 results: | 13.21% ▲ |

ROTH account Net-Liq value

Monthly dividend Income:

ROTH monthly dividend income

ROTH annual dividend income

My dividend holdings:

ROTH monthly options income

ROTH annual options income

Our business account is very extended and over the limit. That means we couldn’t trade this account much. Mostly managing existing trades. We have many trades from 2016 and early 2017 when I was trading aggressive at the money strangles against stock of a questionable quality. These stocks are now hunting me. Overall, our year 2017 was good as the account finished 125.35% up. However, our annual income was lesser than in 2016.

In 2016 we made $19,054.12 in options premiums.

In 2017 we made $13,432.54 in options premiums.

Most of the money were used to pay of the business loan, thus the income had a very little impact on net liq value of the account and the account actually ended flat for 2017 (up $187.72 or 0.82%). But I am happy with the result. In the next year we plan on reducing the current risk and even start trading small trades again and bring the account in line with our rules.

| December 2017 net liq: | $23,114.07 ▼ | (down by -$1,953.38; -7.79%) |

| December 2017 options: | -$904.00 ▼ | (down from previous $2,094.64; -3.91%) |

| XIRR: | -24.82% ▼ | |

| 2017 results | 0.82% ▲ |

Month-to-moth trading results

(The red dots on the chart indicate income estimate, blue bars actual earnings.)

TD account net-liq

Lending Club account got a hit by one note late (now 61 – 120 days; and I expect it to default) but it started growing again. Yet my intent not to add more money remains unchanged. Until I can see the account going up by its own reinvesting what I already deposited I will keep it on an ultra passive mode.

| December 2017 net liq: | $501.29 ▲ | (up by $1.88 0.38%) |

| December 2017 interest: | $11.84 ▲ | (down from previous $8.89) |

| XIRR: | -5.44% ▲ |

Lending Club account net-liq

Our Traditional IRA account is the only account performing well and according to our rules and strategy (ROTH was still an adjustment account in December 2017).

As the strategy says, our goal was to trade options, not to exceed 50% of available buying power, and use 50% of options income to purchase high quality dividend stocks.

I am happy to say that all these principles were followed to the T.

Although this account is a cash account, we could achieve $1,780 average monthly income trading spreads. It is a better result than in our business trading account!

| December 2017 net liq: | $90,487.60 ▲ | (up by $1,913.41 2.16%) |

| December 2017 options: | $2,442.00 ▲ | (down from previous $2,567.00) |

| CAGR: | 19.68% ▲ |

Stocks purchased in December 2017:

none

IRA account net-liq

IRA dividend income

IRA stocks holdings

I hope your December trading was great as ours and we wish you Happy New Year 2018 and a lot of trading success in the new year.

If you like your trades, you can go to our page Trades & Income and see all the trades online on that page. The trades are also posted on our Facebook Page as soon as the trade is opened.

On the page, we post new trades tagged as “NEW TRADE” and all old open trades are then tagged as “OPEN”. That way you will be able to quickly see which trade is new and which is an existing old, open, trade. We change the tag every evening from “NEW TRADE” to “OPEN” so it should be easy to track.

All closed trades are then tagged as “CLOSED – WINNER” or “CLOSED LOSER” so you can also see the results of each trade. When a trade is closed, it is also announced on the page right away and if you follow the page, you should be able to catch it.

Before you start trading (mirroring) our trades, do so in a paper account first and make sure you understand the mechanics and rules of each trade. You can ask questions if you need a trade explanation. Make sure you fully understand the strategy we trade. Later on, you can modify your strategy and start trading on your own.

Hope this helps and good luck!

How was your 2017 trading and investing? Successful? So – so? Or did you lose money?

|

We all want to hear your opinion on the article above: No Comments |

Any time you seek financing for a large purchase, you assume some kind of risk. For example, when you apply for a car loan, you assume the risk that you could be buying a lemon. Similarly, getting a home loan means taking on the risks of home-ownership costs and maintenance. Along with this kind of maintenance is remodeling. If you are thinking about remodeling your home, you may be wondering if the risk associated with financing the expenses is worth taking, and what you can do to possible reduce the risk. Below looks at some of the considerations that can come with this kind of financing.

Remodeling your home can make the style of your house and overall property more modern and attractive to you and any potential buyers. In the event you decide to sell your home at a later date, your remodeling efforts now can help you to potentially sell your home more quickly and for top dollar. Many remodeling projects increase property value, and some may even help you to reduce energy consumption, maintenance costs, and more. Houston Window Experts say insulated windows that regulate heat exchange can save homeowners up to 20 percent in heating costs.

While there is a cost associated with remodeling a home, you can see that there are quite a few financial benefits that you could enjoy as well. Remember that remodeling may also eliminate the need to move into a new space, and there is potentially financial savings associated with this factor as well.

Despite these benefits, there are also risks associated with financing home remodeling efforts. For example, you could default on your financing and potentially lose your home through a foreclosure. You can eliminate this concern entirely by taking out an unsecured personal loan rather than a mortgage against your home. You can also focus on remodeling areas of the home that may have a more significant impact on property value. For example, the bathrooms and kitchen often have a higher return on investment than other areas of the home. Choose materials and a design that is attractive to the masses so you can sell the home quickly if the need arises.

Financing your home remodeling project does have its risks, but you can see that it also has substantial benefits. In addition, there are different ways to mitigate many of these risks. Approach your remodeling efforts with these concepts in mind to make the most out of your plans. As you prepare to remodel your home, pay close attention to the financing options available as well as the details of your remodeling plan. Your focus and attention on these two critical areas can help you to maximize the benefit of remodeling while keeping your exposure to risk in check.

|

We all want to hear your opinion on the article above: No Comments |

I like movies and documentaries about trading and investing. Here are some of my favorites (Episodes One & Two).

[fvplayer src=”https://hellosuckers.net/wp-content/uploads/movies/TMM1.mp4″ splash=”https://hellosuckers.net/wp-content/uploads/2017/12/tmbtmS2.png” width=”450″ playlist=”https://hellosuckers.net/wp-content/uploads/movies/TMM2.mp4,https://hellosuckers.net/wp-content/uploads/2017/12/tmbtmS3.png”]

If you want to see more videos, visit our video archive.

|

We all want to hear your opinion on the article above: 2 Comments |

My goal is simple – continue trading mechanically, like a robot, trade more and small trades. Perfect my patience and discipline trading according to rules and strive to stay away from trades which would cause over trading or imply discomfort as sometimes I tend to jump the gun.

My IRA account is well on track with this and my goal is to maintain $2,000 monthly income in this account and building dividend growth portfolio. Reach $120,000 by the end of 2018.

My ROTH account needs improvement as I have a few bad trades in it, so I will focus on managing them and eventually remove them by the end of the year either as small winners or break even trades. I want to reach $300 monthly income in 2018 (I have only about $4,000 cash available for options trading in this account all else is in long dividend stocks).

My TD trading account is full of mess right now. I have too many bad trades in it, so my goal is again to manage them and eventually remove them. Also start trading small trades to start generating income. I will be happy for at least $100 monthly income in this account, preservation of the account value, and removal bad trades as either winners or break even trades. If losses are taken then they must be offset by other winning trades. My goal is to be able to remove majority of the bad trades and raise available cash to $5,000 by the end of 2018.

TW60 account is a new margin account and I dedicated it to Jesus Christ and our church. I am a strong believer in generating everlasting income so if I can choose whether to donate money which are spent and gone for good or invest them and generate income on that money which can be then spent forever, I would choose the latter one. So in 2018 I am starting with $300 account value (I know it is a very small one) and slowly trading it up and donate all proceeds from the account. Later on I plan on asking the church to open a tax free account and I will move this money to that account but before I do so, I want to have a track record for them to show.

|

We all want to hear your opinion on the article above: No Comments |

Recent Comments