The newspaper industry has experienced steep declines in sales over the past few decades, causing them to be less attractive in the eyes of investors.

Many newspapers have merged, or have been acquired, while others have simply gone out of business. I took a look at a few of the larger companies, and came away with mixed feelings. While their efforts to improve are positive, their financials still are worrisome.

Let’s take a look at some of the happenings in the industry right now.

· Gannett

First up is Gannett (NYSE: GCI), the publishing company that owns USA TODAY. Look no further than the buying binge that it’s been on to see that it is well capitalized as a force in the industry.

Gannett has completed several impressive acquisitions of newspapers throughout the country. They include buying Journal Media Group, which owned the Knoxville News Sentinel, The Commercial Appeal in Memphis, and 13 other newspapers in Tennessee.

Now Gannett has set its sights on Tribune Publishing Company (NYSE: TPUB), which owns the Chicago Tribune, the Los Angles Times and the Orlando Sentinel. Gannett is facing a problem in acquiring Tribune Publishing, however – Tribune Publishing has declined several offers.

The latest offer is $15 per share, which represents a 99% premium to the $7.52 closing price of Tribune’s common stock on April 22, the last trading day before Gannett publicly announced its initial offer for Tribune Publishing. That values Tribune Publishing at roughly $864 million.

On Friday, Gannett sent Tribune shareholders a letter asking them to send a “clear and coordinated message” to their Board that “they expect superior and certain value for their shares and that the Tribune Board should substantively engage immediately with Gannett regarding Gannett’s offer to acquire Tribune for $15.00 per share in cash.

Tribune shareholders will meet on June 2.

When Gannett reported its first quarter revenues for 2016, operating revenues for the quarter were $659.4 million compared to $717.4 million in the prior year, a decrease of $58 million or 8.1%.

It was able to boost digital-only subscriptions by 37%. The company is also enjoying revenue from diversified businesses. That it has acquired and that includes Cars.com and CareerBuilder.com

As far as guidance, the company said it expected full year revenue trends to improve over 2015 driven largely by growth in digital. Advertising revenues were expected to decline in the 5% to 7% range and circulation revenues were expected to decline in the 2% to 4% range.

So while I think Gannett is among the strongest in the business considering its ability to make acquisitions, it will be important to pay attention to how these efforts affect its top and bottom lines.

· Tribune Publishing

On Friday, Tribune Publishing said that Gannett’s statements are misleading. On that same note, Tribune says it is studying the $15 per share offer.

Tribune Publishing boasted $398.2 million of revenue during Q1 2016, which was flat compared to $398.3 million of revenue generated during Q1 2015.

It did suffer from a slip in advertising revenues, which were down 4.4% to $215 million. Circulation revenues of $122 million were up 11.4% in the quarter compared to the prior-year quarter and increased 1.7% from last year. Total digital revenues for Q1 2016 were $55 million, which was an increase of 15% from the prior-year quarter.

Tribune CEO Justin Dearborn said the first quarter results were driven by good momentum in digital and increased circulation revenue offset by a decline in advertising revenue.

To deliver value to shareholders, Dearborn noted that the company was at the “very early stages” of executing its plan to transform the company by increasing monetization of its “important” brands, capitalizing on the global potential of the LA Times, and significantly accelerating the conversion of content to revenue through an enhanced digital strategy.

However, of note is that the company’s second largest shareholder, Oaktree Capital, disagrees with that strategy. The company’s vice chairman, John Frank, noted in a letter, that the turnaround plan is risky and far behind those of competitors in the media business. Saying that the turnaround plan could destroy shareholder value, Oaktree wants Tribune to accept Gannett’s offer.

· News Corporation

News Corporation (NASDAQ: NWSA), which owns The Wall Street Journal, also suffered from a decline in advertising revenues.

It reported its Q3 2016 earnings for the quarter ending March 31 on May 5. Its revenues were $1.9 billion compared to $2 billion for the same period in 2015.

I’d keep an eye on News Corp. because I think its diversification of revenue streams will help mitigate the effects of lower advertising revenue. At the forefront for it is are efforts to improve and expand its digital properties.

· In conclusion

Companies that own newspapers, but that also have diversified products, should be viewed more favorably than those that simply own newspapers. Depending solely on the revenues from newspapers (that are more likely to be used to line bird cages) is a recipe for more disaster for publishing companies. If you sample the newspapers that have gone by the wayside, you’ll likely find that they relied heavily on subscriptions and ad revenue.

Relying on subscriptions is very dangerous considering consumers are cancelling them in droves as they can find their news online. Take the dust up over Facebook this week from critics saying the social media site was blocking conservative news. Newspapers don’t have to be a dying breed. Their owners just have to find other revenue streams, such as those from digital products, and even other businesses, to deliver the best in shareholder value.

|

We all want to hear your opinion on the article above: No Comments |

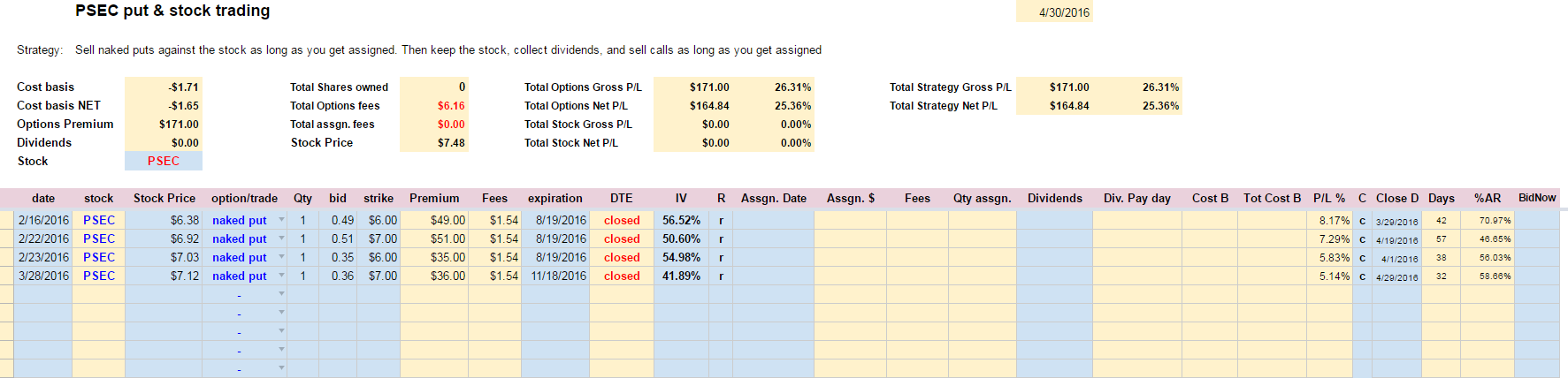

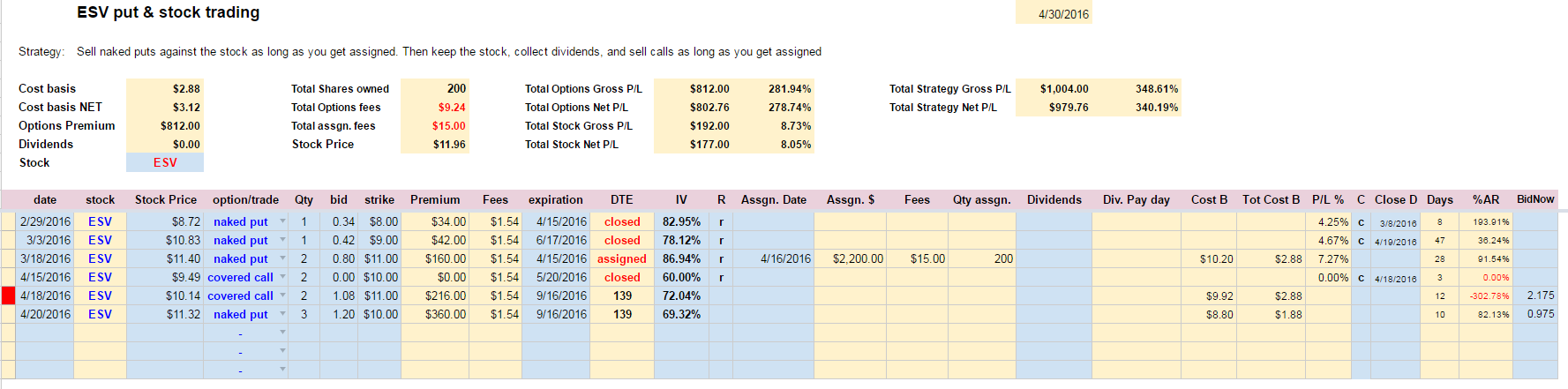

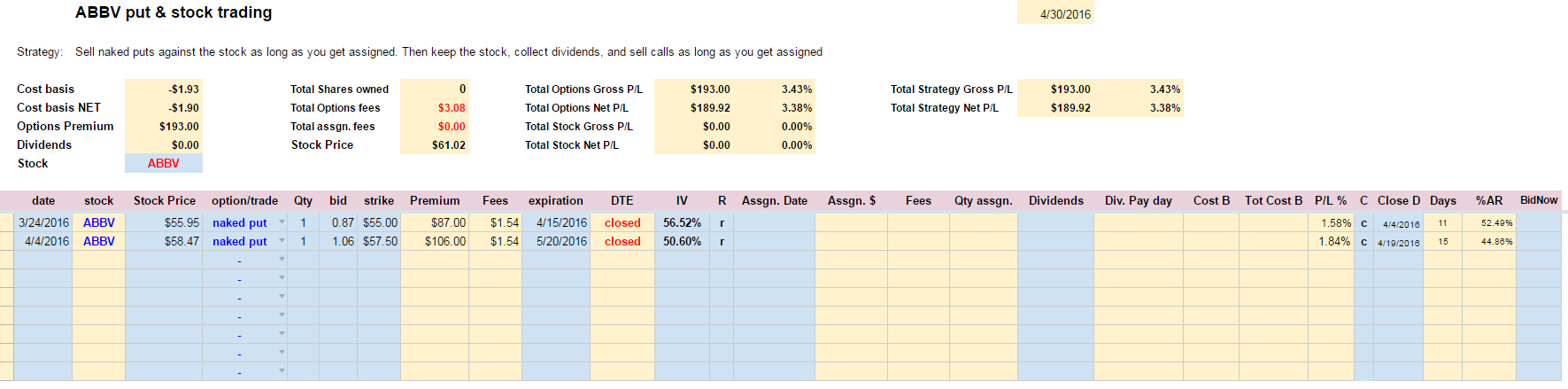

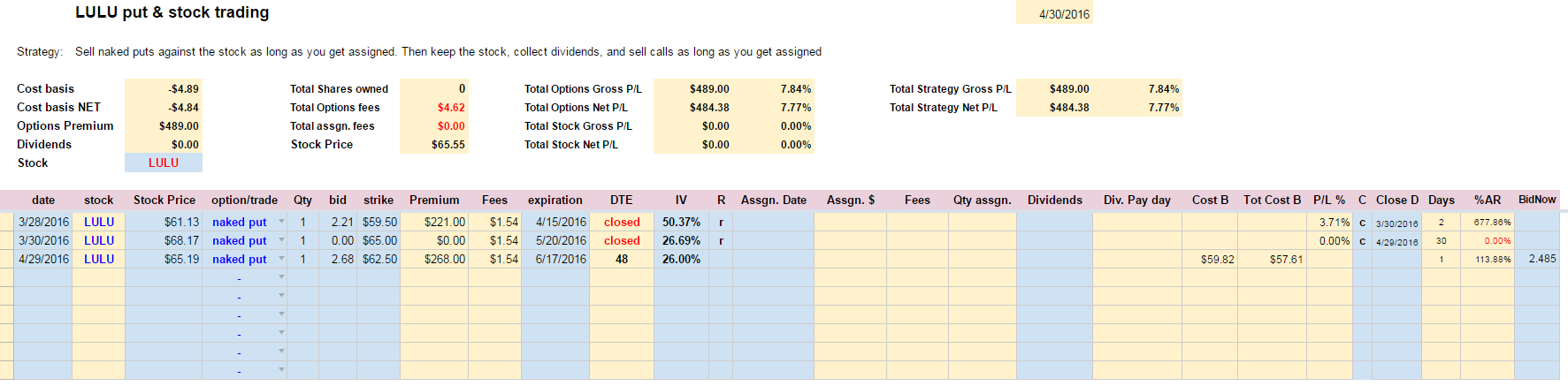

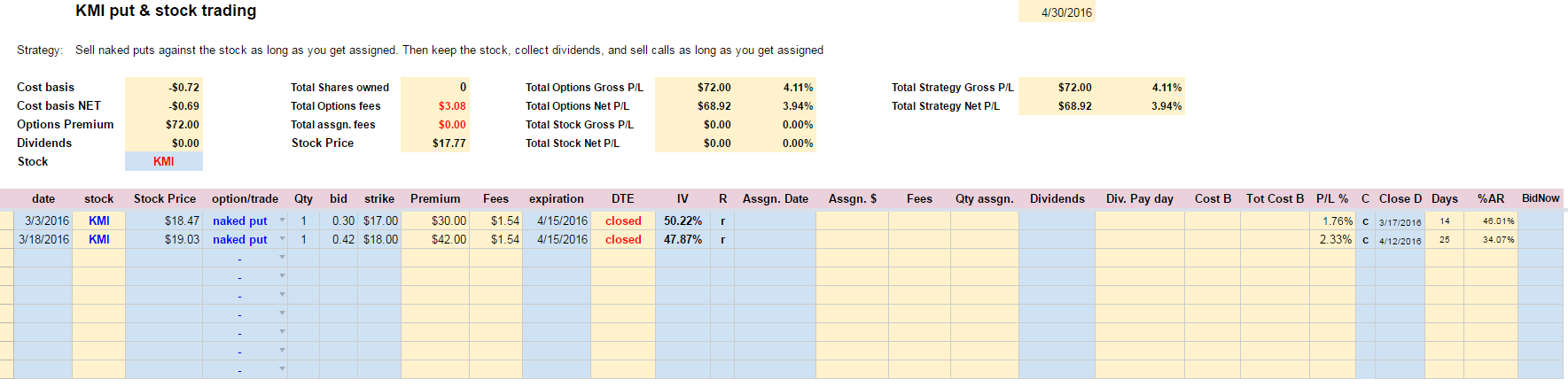

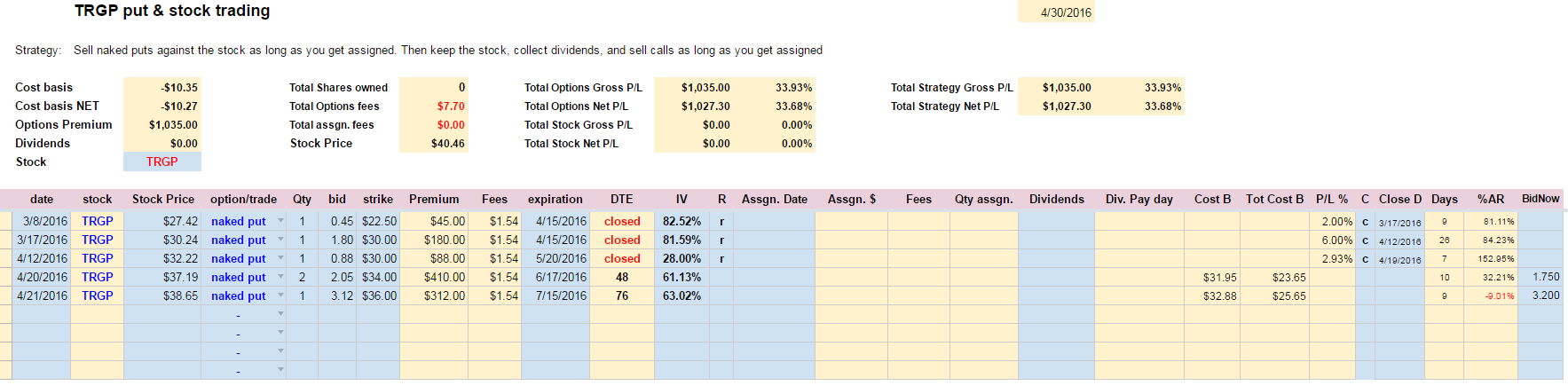

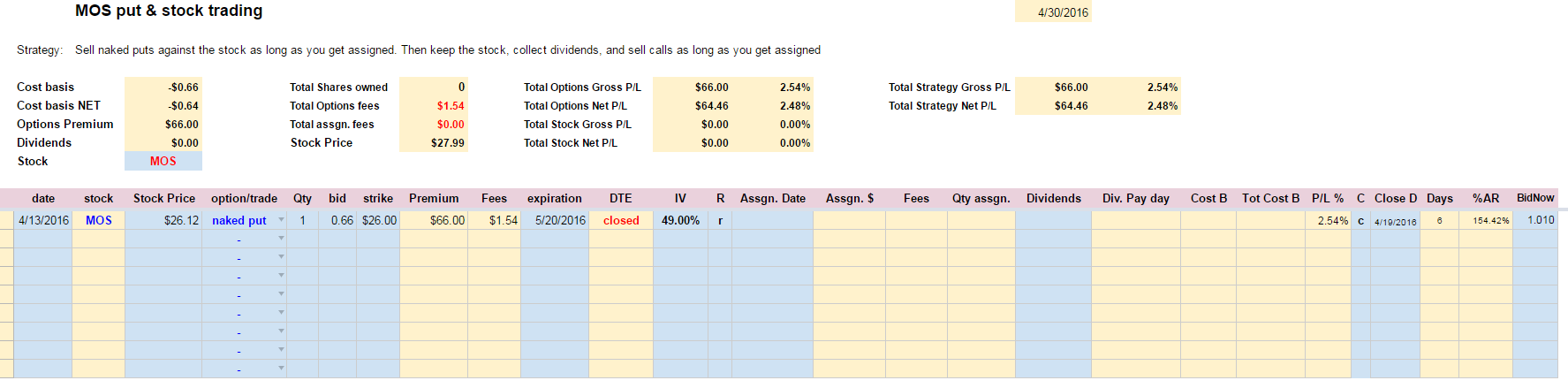

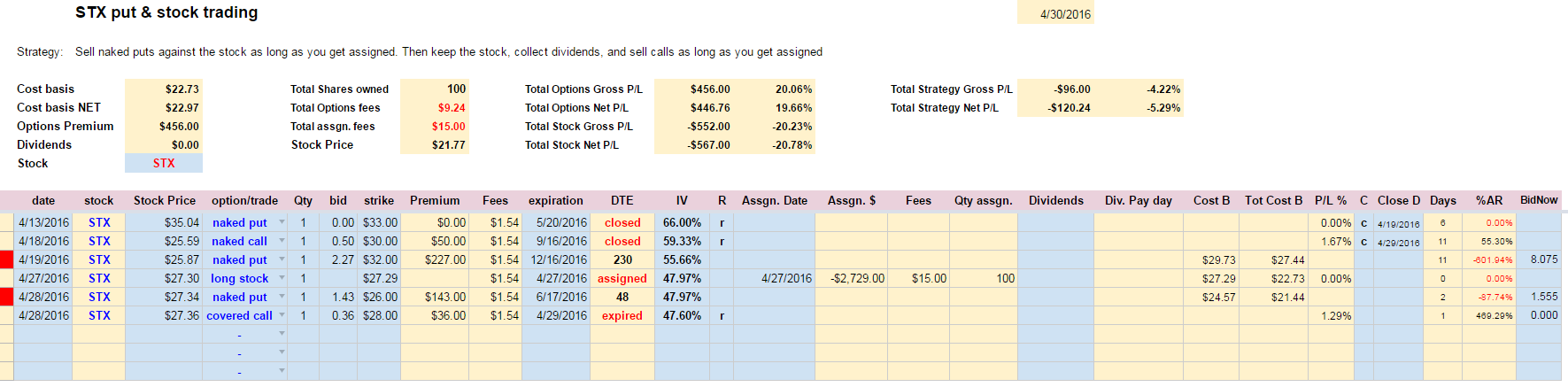

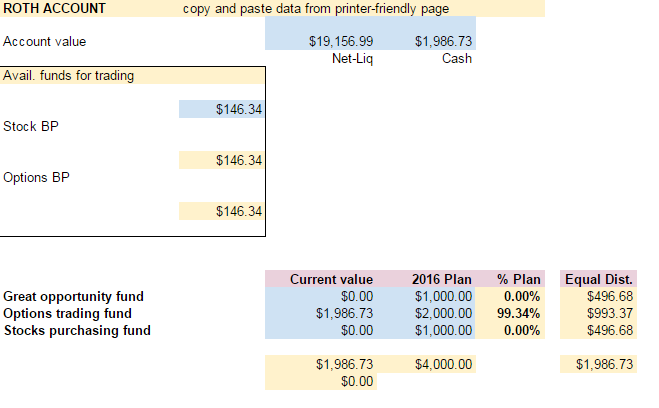

You know it. You sell a put option and the trade goes busted next day. If you have never experienced this, then you are still going to. That I can guarantee.

You know it. You sell a put option and the trade goes busted next day. If you have never experienced this, then you are still going to. That I can guarantee.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Recent Comments