I decided to take a loss at my Armour residential put selling trade. Originally I believed in this stock, but lately I consider Armour residential a junk every dividend investor should avoid.

There is plenty of investor out there I could see who think this stock is a great value because of its book value (BV) is at around 5.43, it pays dividends (currently $0.07 a share) and who knows what else.

In the past I was buying this stock (you can see my trades in the ARR archive) and enjoyed dividends this stock was paying.

I even started selling puts to generate more income because I was OK to buy more shares in case of assignment.

But then situation changed.

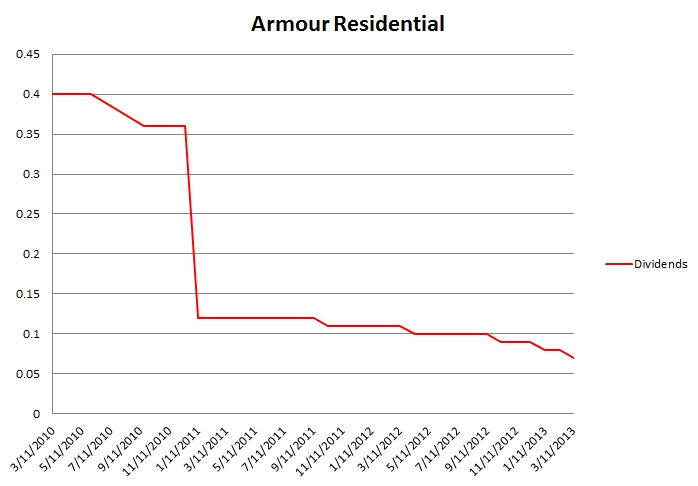

ARR started cutting its dividends. In 2011 the company paid 0.11 a share monthly dividend. It kept on that level for some time, but then started cutting it. For a dividend investor this should be a reason to sell the stock. No exceptions, no reasoning, no discussion. Yet I was ignoring it and continued buying. I too was excusing myself, that mREIT is a different beast and all this can be temporary.

Then the management issued an SPO (secondary public offerings) to further damage investors. People out there will tell you that that is how mREITs work, how they get their money. Well, I would agree on that if the management wouldn’t wait for the stock price to climb from $6.5 a share up to $7 a share to issue SPO. Once SPO was out the stock plummeted back to $6.5 and never recovered.

Many out there were saying that this was ruthless step from the management ignoring shareholder and that they did this just to collect nice fees, which were tied to how much cash they were able to raise. Why would a management not care? It’s because ARR is managed externally by a private company Armour Residential LLC. Thus they are milking Armour Residential fund as much as they can. Their primary interest is their own company and their own beings. The fund is just a cow to them and they do not care that there were investors giving them money.

I still was OK with that. I still thought, that this was overreaction from the market and tough times in real estate and mortgage markets and this will be overcome over long period of time.

And then, short after SPO another dividend cut came. This time from 0.09 to 0.08 a share. I suffered one cuts from 0.12 down to 0.10, 0.09, and 0.08 during my holding period since March 2011 when I first bought this stock. that was enough even to my excuses and I sold.

Lucky enough, because then the stock plummeted after yet another dividend cut from 0.08 to 0.07. I sold at $6.5 a share and thanks to collected dividends I got out break even. Since then the stock trades at $4.45 a share as of this writing. A 50% loss!

I still got stuck with a short put in my account

To protect myself I decided to roll the put far away in time to avoid potential assignment into stock I no longer wanted. You can see my put trades in this archive.

I sold two puts as far in January 2014. My plan was to let time decay erode the puts as much as possible so I can buy puts back and get break even (at least) or smaller loss.

So why I decided to close this trade prematurely and take large loss?

ARR seems to be doomed and problems are piling. I was watching this stock briefly just to make sure everything went so-so that I could keep puts open. But today I saw that the CEO Jordan Zimmerman stepped down. That can be a good sign when you could see so many bad results this stock was presenting to investors. You could say that a new CEO would do a better job. But the following event convinced me that I didn’t want to have anything in common with this stock.

Arr received a delisting notice from NYSE. If the company doesn’t fix what NYSE has to say by August 12, 2013 (next Monday), it will become delinquent in compliance or to use the notice language “will be deemed non-compliant” or “below compliance” and can be delisted.

What can happen if the stock gets delisted? The stock will move to OTC market and I can get assigned prematurely. And that would be a step I definitely don’t want.

I wasn’t expecting being right all the time, and sometimes I will be taking a loss. This one was one of those trades.

Trade detail

I bought back ARR puts to close the trade:

08/08/2013 11:59:59 Bought 2 ARR Jan 18 2014 7.5 Put @ 3.6

At this point I hold no ARR trade and the ARR file is closed.

We all want to hear your opinion on the article above:

2 Comments |

When I read about Flexible Dividend Reinvestment tool on

When I read about Flexible Dividend Reinvestment tool on

{kind=link}

{kind=link}

{kind=link}

Recent Comments